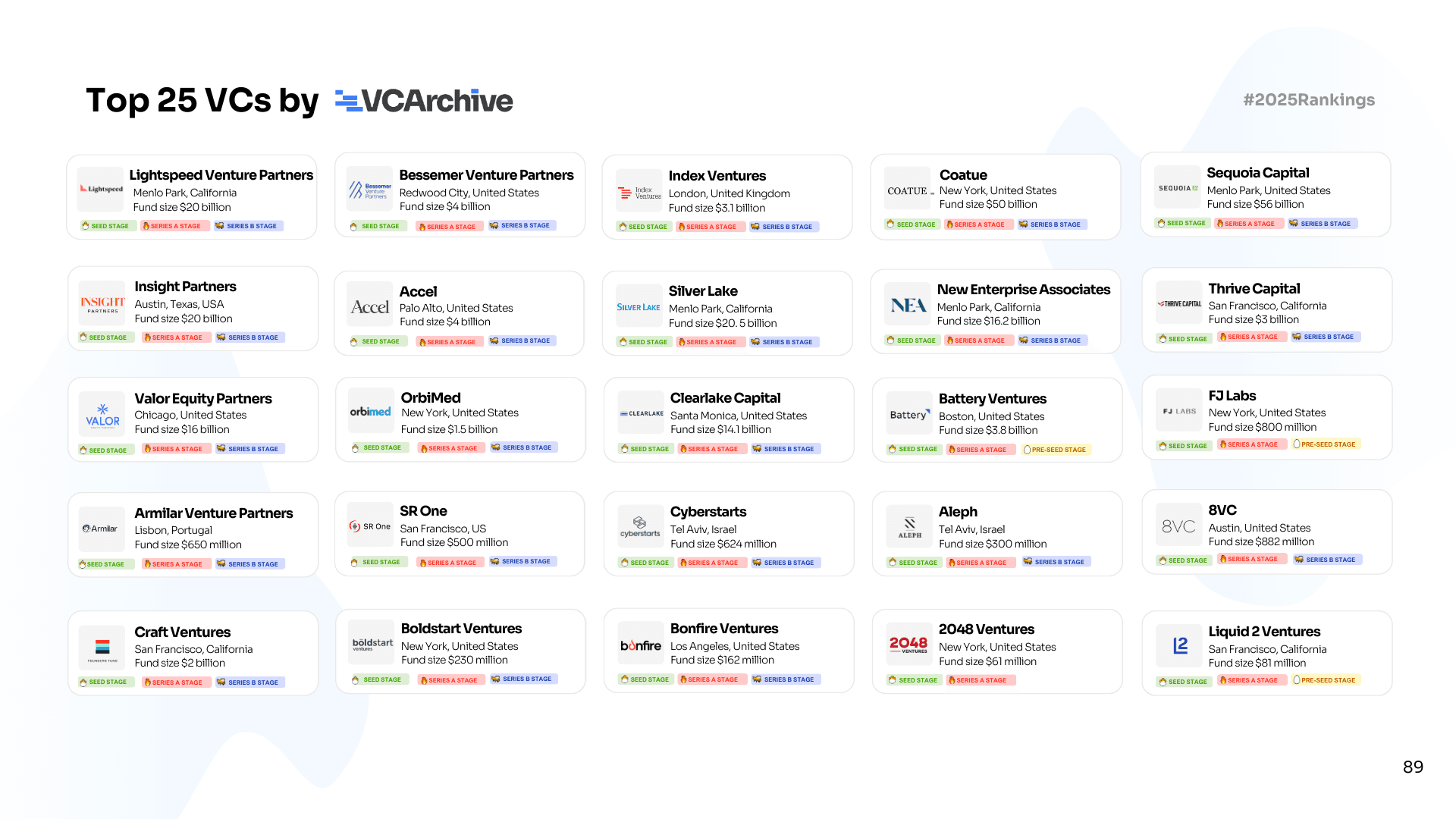

Inside the 1%: The 25 VC Firms That Called the Shots in 2025

75% of all U.S. venture capital raised in 2025 went to the top 30 firms. Nine of those captured half of everything. This isn't consolidation, it's a collapse inward, driven by LP exhaustion after years of watching 2021-vintage funds fail to return capital.

The result is an industry that looks diverse on paper and is operationally controlled by a few dozen players. Understanding which type of firm you're dealing with before you reach out, is the difference between a meeting that moves things and months burned on the wrong target.

The four types operating in this market right now

Compounders:

Sequoia, Bessemer, Accel, Index, Lightspeed, NEA. These firms don't pitch founders anymore. Founders pitch them.

Their edge is time, not size: pattern recognition across market cycles that no new fund can manufacture. Sequoia's follow-on rate of 75-85% is the clearest signal on this list. When they re-invest, it means something. When anyone else does, it might be obligation.

Scale players:

Coatue ($70B, 47% IRR), Silver Lake ($102B, 37% IRR), Insight Partners ($90B), Thrive Capital ($16B, 2.8x multiple). These firms operate at the intersection of public and private markets.

Silver Lake's 1.7x multiple looks modest until you realize they're writing $30-100M checks into established businesses, the absolute capital returned dwarfs most entire venture funds. Insight's 130-person operational platform embedded post-investment is something no generalist can replicate at speed.

Specialists:

Cyberstarts, YL Ventures, Ten Eleven, OrbiMed, SR One. This is where the most interesting performance data lives:

- Cyberstarts: 80% graduation rate, 12 active portfolio companies, seed-only cybersecurity from Tel Aviv. Deep, non-replicable knowledge

- YL Ventures: Four consecutive funds backing Israeli-founded cybersecurity scaling into the U.S. Orca Security, Axonius, Snyk, Island

- OrbiMed: Life sciences only since 1989. Managing partners with PhDs and MDs who have sat through entire drug development cycles

- SR One: Spun out of GSK's venture arm with decades of pharma operating experience. Now autonomous capital unconstrained by corporate mandates The VCA report said it plainly this year: thematic funds are winning. The generalists are the ones under pressure.

Contrarians:

Founders Fund, 8VC, NFX, Valor, G2VP, Angeleno. Defined less by sector and more by going where the consensus won't.

Founders Fund has a 60-70% write-off ratio and a 3x multiple on $12B - most funds would call that catastrophic,

Peter Thiel calls it the price of backing revolutionary technology. 8VC deliberately targets industries most Silicon Valley funds consider too hard: logistics, defense, regulated bio-IT. NFX built an entire thesis around network effects and produced Ramp, DoorDash, Poshmark, and Lyft from it.

Three things worth knowing before you reach out

- Warm intros aren't optional for 7 of these 25 firms. Sequoia, NEA, NFX, Founders Fund, Homebrew, Boldstart, and Index all require introductions. It's not gatekeeping. The Venture Capital Archive's Annual Report documents that nearly 2 in 3 top-20 deals are co-invested alongside another top-20 firm. The network is self-reinforcing by design.

- IRR comparisons across this list are meaningless without context. Coatue's 47% and Silver Lake's 37% reflect completely different risk profiles, check sizes, and holding periods. NEA's 36% across 19 funds means something entirely different from Thrive's 26% across 8. Compare within strategy type, not across the list.

- Portfolio density matters more than founders realize. Sequoia has 500+ companies. Lightspeed has 400+. At that scale you're competing for partner attention against hundreds of founders with more traction and longer relationships.

The smaller specialists - Cyberstarts at 12, YL at 9 active can offer something the platforms genuinely cannot: a GP who knows your business well enough to make one phone call that changes your outcome.

The bubble map above shows all 25 firms sized by AUM, grouped by type. The size difference between quadrants is the story, the scale players occupy a different universe than the specialists. Both matter, but they are not the same conversation.

Full profiles - fund size, check sizes, graduation rates, follow-on rates, portfolio companies, direct contacts at venturecapitalarchive.com.

Research and curation by the Venture Capital Archive team. Data sourced from the VCA Annual Report 2025. All information verified as of 2025.

Inside the 1%: The 25 VC Firms That Called the Shots in 2025

Rows per page