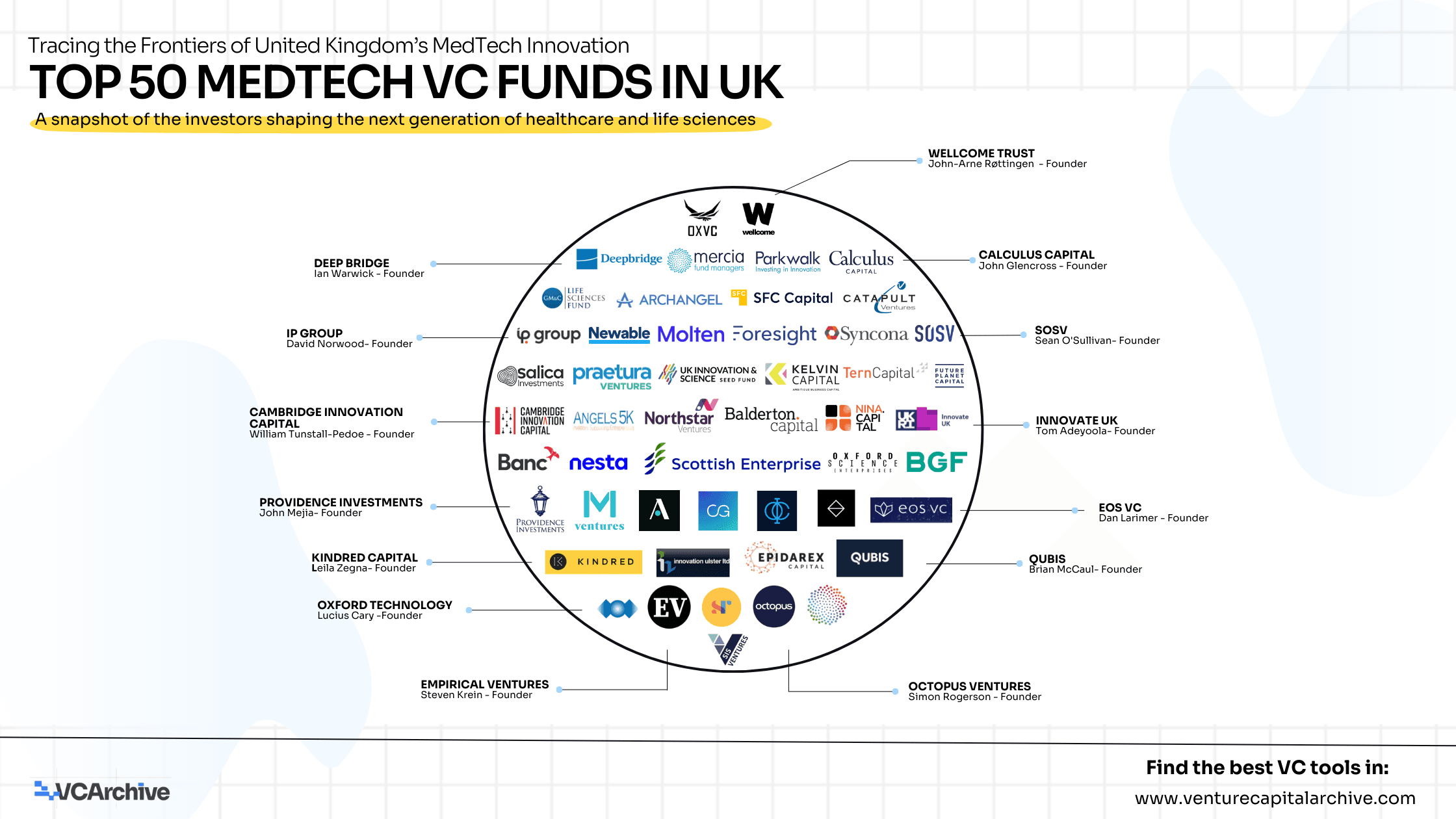

Top 50 Medtech VC Funds in United Kingdom

Below is a deeper look at the landscape, structured not as a directory, but as a map of the different forces shaping UK medtech.

1. The University Translators

Some of the most consequential breakthroughs in UK medtech start far from the market. In physics labs, wet labs, engineering rooms. Few investors know how to translate those discoveries into companies that survive regulatory scrutiny. This is where Parkwalk Advisors, Oxford Science Enterprises, IP Group, Oxford Technology Management, Oxford Investment Consulting, Cambridge Innovation Capital, QUBIS, and Innovation Ulster.

These firms behave more like scientific partners than financial sponsors. They know how to work with tech transfer offices, identify defensible IP, match researchers with commercial talent, and build companies around discoveries that may take years to mature. Without them, the UK would not have such a deep reservoir of medtech spinouts.

What sets this group apart is not simply sector focus, it is cultural fluency. They speak “science” as naturally as they speak “venture.”

2. Scotland’s Medtech Identity

The Scottish ecosystem has undergone a transformation. Not by copying London, but by building something it owns. Scottish Enterprise, Scottish Investment Bank, Archangels, Eos, SIS Ventures, GM&C Life Sciences Fund, Angels 5K, and Kelvin Capital have cultivated an environment where health innovation is anchored in community, research depth, and long-term partnership.

Scotland’s strength is not volume, it’s precision. These funds are highly selective, often supporting companies from inception through multiple funding cycles. They mix public and private capital, pair founders with domain veterans, and co-invest intelligently across early development milestones.

The result: a region once overlooked is now producing meaningful medtech companies with global ambitions.

3. The Early Builders: Investors Who Shape the First 1,000 Days

Deepbridge Capital, SFC Capital, Newable Private Investing, Mercia Fund Managers, SyndicateRoom, Salica, Kindred Capital, Empirical Ventures, and Praetura Ventures all play a different but equally decisive role. They show up when products are half-formed and founders are still figuring out regulatory implications, clinical workflow, or reimbursement models.

Rather than asking for polished metrics, these investors supply discipline, structure, and the first real “yes” that transforms a prototype into a venture-scale ambition. For medtech founders, the early stage is less about capital and more about guidance. These firms anchor that process.

Three things they do that matter:

• Teach founders how to build clinical credibility.

• Help secure first pilots and institutional partnerships.

• Prepare companies for the rigours of a Series A.

4. Scale-Up Specialists: Where Medtech Learns to Compete

Once a company has early validation, it must scale beyond the lab into manufacturing, compliance, sales, and clinical integration. This is where Albion VC, Catapult Ventures, Development Bank of Wales, Providence Investment Company, and Calculus Capital step in.

Their role is less romantic but more essential: creating operational structure. They professionalise reporting, accelerate commercialisation strategies, map regulatory pathways, and connect companies to distributors and health systems.

They are not the loudest funds in the press, but they are often the reason a medtech company avoids failure during scale.

5. UK’s Global Engines: Funds That Turn Startups Into International Competitors

Some investors operate with a very different altitude. Octopus Ventures, Syncona Partners, Molten Ventures, Balderton Capital, Wellcome Trust, and Foresight Group act as global capital platforms. They move companies across borders, anchor late-stage R&D, and put significant capital behind clinical excellence.

These funds have something few others possess: the ability to fund long timelines. Medtech often requires five to ten years of sustained capital before outcomes become visible. This group thrives in that environment. Their networks include pharma giants, regulators, payers, and global manufacturers giving founders access to expansion pathways that simply do not exist at the seed stage.

6. Digital Health and Data Infrastructure: The Fastest-Moving Frontier

The UK’s digital health scene has matured into a serious investment domain. Nina Capital, Crista Galli Ventures, Nesta Ventures, and Tern invest where software meets medicine interoperability, clinical decision support, health-data infrastructure, remote monitoring, and AI-driven workflows.

Unlike traditional medtech, these companies scale more like SaaS. But the stakes are higher than enterprise software: reliability must be absolute, data governance airtight, and adoption clinically meaningful.

This category is expanding fast because three forces align:

• Health systems need automation.

• Clinicians need better tools.

• Patients demand convenience and transparency.

7. Public-Private Catalysts: When Government Makes Venture More Resilient

Innovate UK remains one of the most powerful accelerators of scientific innovation in the country. Grants, non-dilutive funding, and knowledge networks reduce the technical risk of early medtech development. Business Growth Fund and Development Bank of Wales provide long-term capital that many SMEs cannot access from private markets alone.

This infrastructure doesn’t simply support startups, it stabilises the entire ecosystem. In medtech, where R&D timelines are long, this stability makes the UK uniquely competitive compared to ecosystems dependent solely on private capital.

8. Investors With Unique Philosophies and Alternative Models

Not every investor fits into classical categories. Some have built distinctive strategies that influence the overall medtech landscape:

• SyndicateRoom uses data-driven cohort investing, reshaping how early-stage risk is shared.

• Angels 5K, Kelvin Capital, and Eos Advisory combine angel experience with institutional rigour.

• Molten Ventures, Future Planet Capital, and Syncona Partners specialise in supporting companies through late-stage scientific inflection points.

• Business Growth Fund invests minority capital in profitable health-related SMEs - an uncommon model in VC.

These alternative approaches create diversity in the funding environment, which is essential for a sector as complex as medtech.

What All This Means for the UK Medtech Future

The Top 50 Medtech VC Funds in the United Kingdom do not form a single ecosystem, they form multiple ecosystems that interlock. This layered structure is why the UK consistently produces companies that punch above their weight globally. It is why scientific discoveries turn into viable products, why founders find mentorship at every stage, and why even small regions can create globally relevant medtech ventures.

Explore the full list of Top 50 Medtech VC Funds in United Kingdom, including their sector focus, stage, fund size, and global HQ - now live on VCArchive.

Top 50 Medtech VC Funds in United Kingdom

Rows per page