New Venture Funds - May 2026

The bifurcation nobody is saying out loud

Something uncomfortable is happening in venture capital and most people in the industry are dancing around it rather than naming it directly.

Abundance at the apex and measured scarcity elsewhere. The middle is marked by growth strategies that once thrived on modest multiple expansion but has largely thinned out. Higher capital costs and ruthless pricing leave little room for alpha. But this clarity is a feature, not a bug.

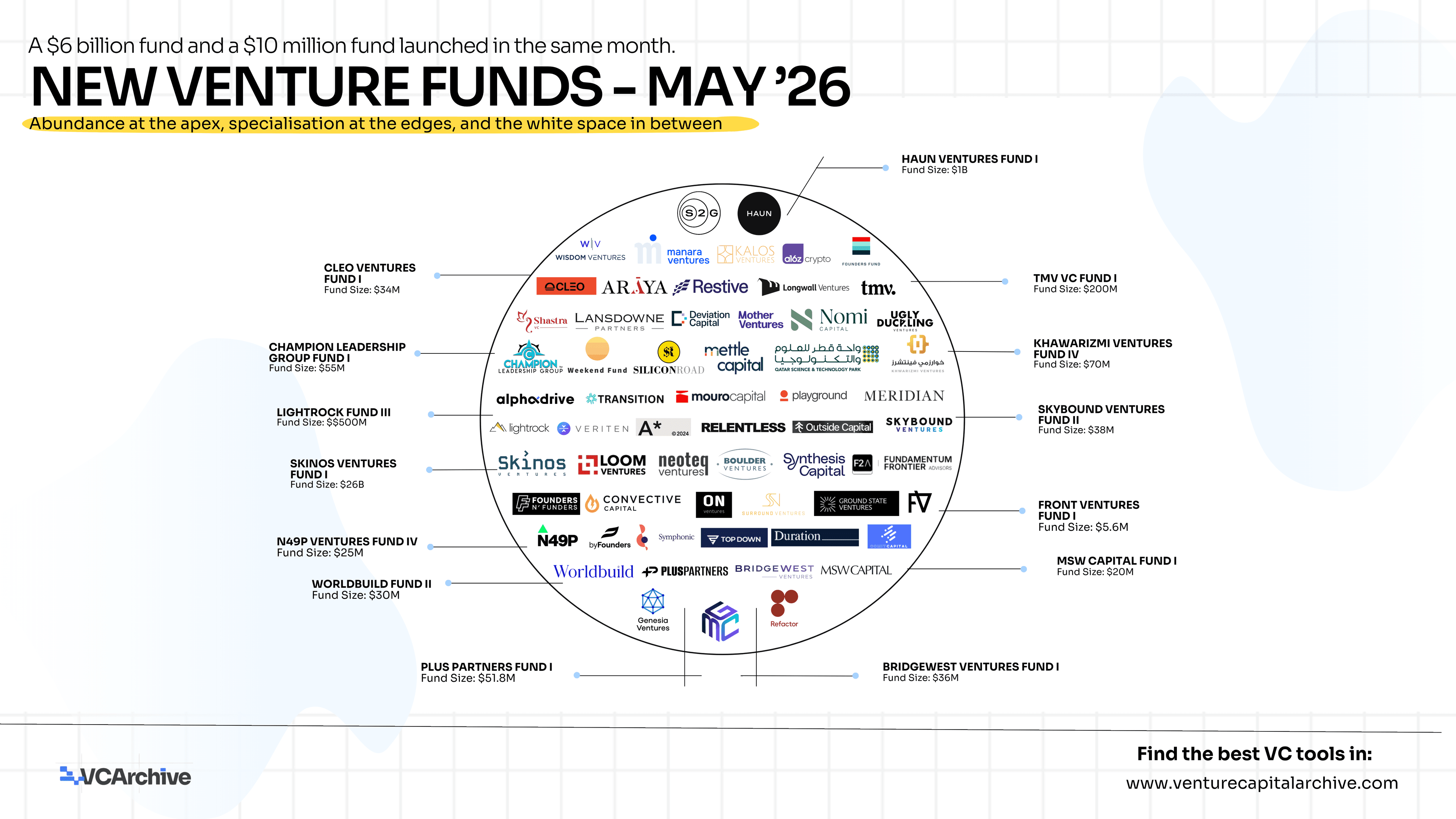

The clearest possible illustration of that dynamic is May 2026's new fund launches. In a single month, Founders Fund closed at $6 billion and Mother Ventures closed at $10 million. Both are rational. Both are correct. Both are responses to the same market and they are responses to completely different parts of it.

Understanding why both exist simultaneously, and what each one tells you about the state of the asset class, is more useful than any amount of macro trend analysis.

What a $6 billion fund is actually saying

When Founders Fund closes at $6 billion, it is not making a bet on the venture capital market. It is making a bet that it can access a small number of extraordinarily important companies at the right stage and own enough of them to generate returns that justify the capital.

The venture capital landscape in May 2026 reflects a strategic pivot toward verticalized autonomy embedding high-level AI capabilities into legacy industrial sectors that have historically resisted digital transformation. Capital is increasingly flowing toward companies that solve the last mile problem in AI implementation.

That is not a seed-stage thesis. That is a platform thesis. It requires the brand, the network, the existing portfolio relationships, and the ability to write checks large enough to matter at Series B, C, and growth. Only a handful of funds on earth can execute it. The ones that can are raising very large vehicles because the opportunity they see is genuinely very large.

Concentration in top-tier assets persists. The 2026 venture environment will reward selectivity and conviction. Critically, the hyperfocus on AI has had widespread impacts on fundraising for other sectors — only companies with the strongest competitive positions are attracting substantial funding.

The $6 billion funds are not hoarding capital. They are positioning for a small number of very large outcomes in a market where very large outcomes are increasingly where all the value creation is concentrated.

What a $10 million fund is actually saying

Mother Ventures in New York raised $10 million specifically to back maternal health and femtech founders. That is not a hedge against the AI mega-trend. It is a deliberate choice to occupy a corner of the market that $6 billion platforms will never efficiently serve.

This is the more interesting story in May 2026's fund landscape, because it represents a genuine innovation in how venture capital is being structured.

For emerging managers, the bar has risen significantly. Fewer firms are entering the market, while others are exiting due to fundraising challenges. Closing a second vehicle has become a significant challenge, especially where past performance is harder to prove amid long hold times.

And yet the emerging managers on this month's list kept raising. Here is why that is rational.

A $10 million fund does not need a $500 million exit to return capital. It needs a $50 million exit, or several $20 million ones. Those outcomes exist in abundance in categories that mega-funds structurally cannot pursue; femtech, outdoor recreation, care tech, workforce technology for underserved communities, beauty and wellness DTC brands. The US has made headlines with disproportionate AI megadeals, but the early part of 2026 has also demonstrated that capital still exists across sectors, it has simply become more concentrated and more selective about what it backs.

The small specialist funds on this list are not competing with Founders Fund. They are exploiting the white space it creates.

The geography of May's launches tells you where the next wave is forming

Look past San Francisco and London and the month's fund launches reveal something important about where conviction capital is forming in parts of the world that most VC coverage ignores.

The Middle East is becoming a serious LP and GP market simultaneously.

Global Millennial Capital closed at $100 million in Dubai backing fintech, SaaS, and AI across emerging markets. Khawarizmi Ventures raised $70 million in Dubai for fintech and digital health across MENA. QSTP Tech Venture Fund anchored Qatar's deep tech ecosystem with $30 million backed by Qatar Science and Technology Park. These are not tourist capital vehicles. They are the beginning of a genuine regional venture infrastructure that will compound for decades.

Israel is building its next generation of deep tech funds.

Playground Ventures closed $475 million in Herzliya for hardware, robotics, AI, and semiconductors - a fund size that would be notable in San Francisco is extraordinary for the Israeli ecosystem and signals the maturation of what has long been called the Startup Nation into something more like a Deep Tech Nation. Surround Ventures and Commit Capital represent the earlier-stage layer of the same ecosystem.

The Nordics are building European-scale conviction funds.

byFounders in Copenhagen closed $148 million for European and Nordic founders across AI, climate tech, and enterprise software - a vehicle that reflects the Nordics' consistent ability to punch above their geographic weight in startup quality while remaining systematically underfunded relative to London and Berlin.

India is building dedicated deep tech infrastructure.

Shastra VC in Bangalore raised $100 million specifically for deep tech, AI, robotics, semiconductors, and quantum computing, categories that Indian founders have historically struggled to raise domestically and that global funds have struggled to evaluate without local expertise.

The three most interesting theses in this month's list

Vertical AI is the new SaaS

Almost every generalist fund that launched in May has AI in its focus areas. That is expected and largely unremarkable. What is more interesting are the funds pursuing genuinely vertical AI theses, AI embedded into specific industries with specific customer bases and specific go-to-market strategies.

Kalos Ventures in Atlanta raised $78.8 million specifically for workforce tech, care tech, education tech, and aging tech, the kinds of labour-intensive service industries where AI-driven automation creates the most dramatic efficiency gains but where most Silicon Valley VCs have the least customer relationships and market knowledge. Veriten in Houston raised $105 million dedicated to energy transition and oil and gas technology - an industry that controls trillions of dollars of assets and is in the middle of the most consequential technology-driven transformation of its history, yet remains systematically underserved by venture capital because most GPs do not understand it.

The specialisation of consumer capital

The consumer VC landscape of 2026 is not one market. It is a dozen distinct markets, each requiring different expertise, different networks, and different return models. This month's launches reflect that.

Skinos Ventures in London raised $26 million for beauty, wellness, and femtech DTC brands - a category that generates enormous consumer loyalty and surprisingly durable unit economics but that generalist funds consistently mis-evaluate because they apply software metrics to physical product businesses. Relentless in London raised $80 million for consumer brands, sustainable goods, and lifestyle tech. Outside Capital in Boulder raised a fund dedicated entirely to the outdoor recreation industry - a market worth hundreds of billions of dollars that has been almost entirely ignored by institutional venture capital.

Champion Leadership Group in Atlanta raised $55 million for consumer brands, sports, and wellness with a specific focus on underrepresented founders, combining category specialisation with a sourcing advantage in communities that most coastal funds do not have meaningful relationships with.

Defence tech is going global

Front Ventures in Stockholm raised $5.6 million for defence tech, aerospace, and drones - a tiny fund with an outsized significance. It represents the European recognition that defence technology investment cannot be outsourced to American funds if European nations want sovereign capability in the technologies that will define the next era of security. AlphaDrive Ventures in San Francisco raised $100 million for cybersecurity, AI, and national security with a team that includes former intelligence community professionals. Together they represent opposite ends of the same global trend: defence tech venture capital is growing, professionalising, and internationalising faster than almost any other category in the asset class.

What founders should actually do with this

Giant AI rounds do not mean the market is easy. New funds do not mean every founder is suddenly fundable. The market is rewarding clarity, concentration, and conviction. Sharpen your category. Tighten your proof. Reduce your burn. Build investor fit before outreach. Make your company easy to understand without making it simplistic. That is the game in May 2026. Not louder fundraising. Better fundraising.

The practical implication of a month that produces both Founders Fund at $6 billion and Mother Ventures at $10 million is that the question every founder needs to answer has become more specific, not less: which of these 60-plus funds is structurally capable of writing me the right check at my stage, in my category, in my geography, at my moment?

A founder building maternal health technology does not need Founders Fund. A founder building AI infrastructure for the enterprise does not need Skinos Ventures. Getting this mapping right before the first email goes out is the difference between a fundraising process that closes in eight weeks and one that drags for a year without a term sheet.

The 60-plus funds in the May 2026 VCA list represent the full spectrum of new capital that was committed in a single month, the platforms, the specialists, the geographic pioneers, and the category innovators. Read it as a map, not a menu. The right door for your company is specific, and finding it is the work worth doing before everything else.

New Venture Funds - May 2026

Rows per page