New Venture Funds - February 2026

Fundraising dropped. LPs pulled back. Emerging managers struggled to close. And for a while, it felt like the entire system was pausing — waiting for clarity that never quite came.

And then February happened.

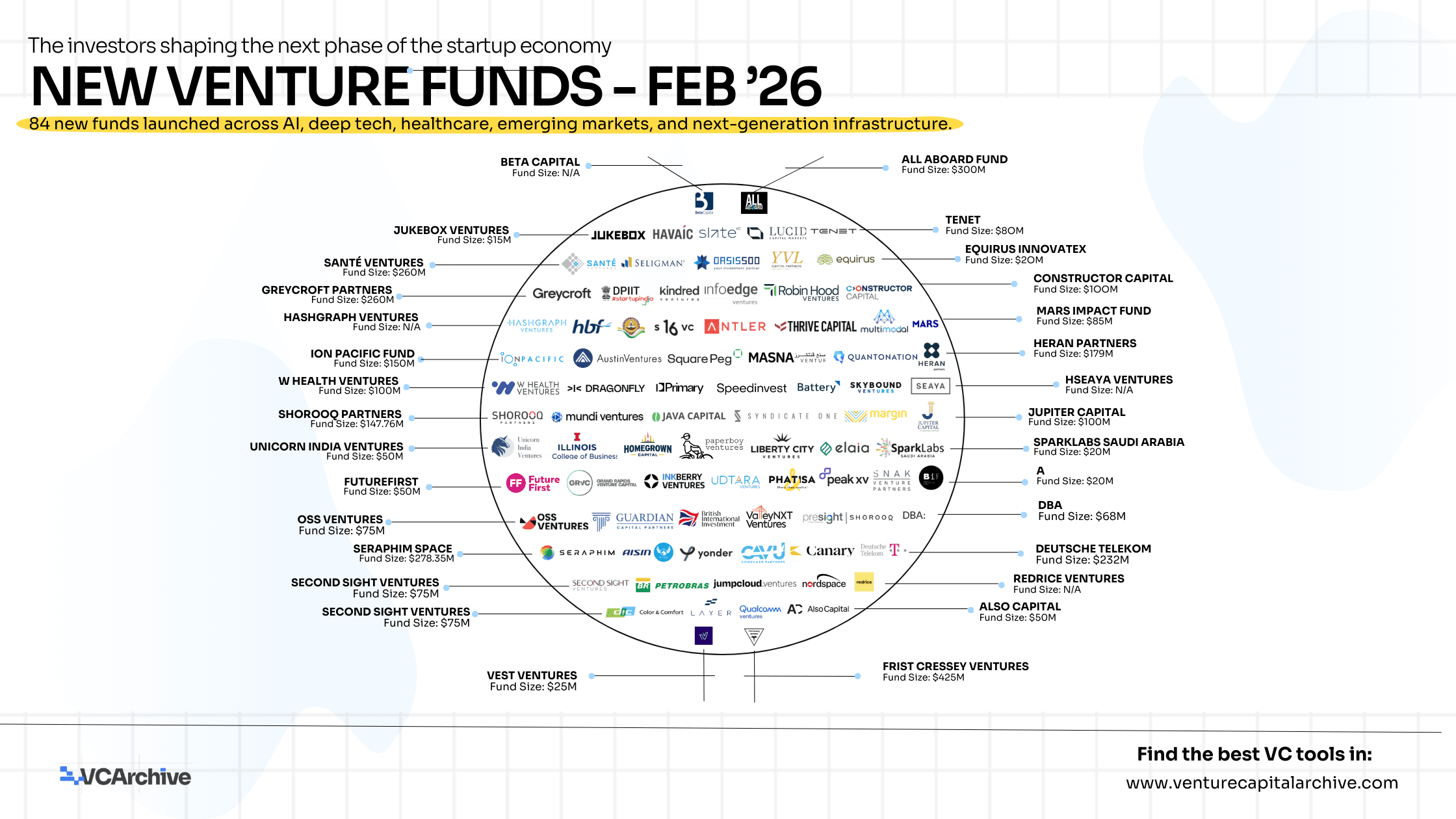

In the shortest month of the year — just 28 days — 83 new venture funds were launched or actively entered the market.

Not quietly. Not passively. But with clear theses, defined strategies, and, most importantly, fresh conviction.

This isn’t just a data point. It’s a signal.

Because venture doesn’t come back all at once. It comes back like this — fragmented, diverse, and full of intent.

What makes this moment different is not just the number. It’s the type of funds being created.

This is not 2021 all over again. There’s no sense of excess, no broad “we invest in great founders everywhere” positioning. What you see instead is something much more deliberate.

Funds like All Aboard Fund are not just backing climate — they’re focused on scaling infrastructure for deployment, solving the hardest part of climate tech. Tenet isn’t another AI fund; it’s built around a very specific idea: that AI will consolidate fragmented industries through roll-ups. Masna Ventures ties directly into Saudi Arabia’s defense localization strategy, blending geopolitics with venture. And NordSpace Ventures is backing something even more ambitious — a sovereign space ecosystem.

These are not generic strategies. They are context-driven bets on how the world is changing.

That’s the real shift.

At the same time, the definition of who counts as a “venture investor” is expanding.

Some of the most interesting funds in this list are not traditional VCs at all. They are extensions of larger systems.

When Qualcomm Ventures invests, it’s not just capital — it’s access to the global semiconductor and connectivity ecosystem. When Petrobras CVC backs a company, it’s tied to real-world energy infrastructure and decarbonization. The Emerald x DIC Physical AI platform sits at the intersection of materials, manufacturing, and AI — a place where most traditional VCs simply don’t operate.

What this creates is a different kind of venture capital. One that is less about financial engineering and more about strategic positioning.

And for founders, that changes everything.

Because the best investor is no longer just the one who can wire the largest check — it’s the one who can accelerate the system your company depends on.

Geography is shifting too — not in a dramatic, headline-grabbing way, but in something more subtle and more important.

It’s becoming intentional.

India is no longer “emerging”; it’s structured and layered. You see it in funds like Peak XV Partners, Equirus InnovateX, Java Capital, and the Startup India Fund of Funds 2.0 — a mix of institutional scale, early-stage experimentation, and government-backed liquidity.

In the Middle East, funds like Shorooq Partners, YVL Capital, and SparkLabs Saudi Arabia reflect something else entirely: a region that is no longer just attracting capital, but deploying it with its own thesis.

Across Africa, HAVAÍC and Phatisa are not chasing trends — they’re building around real economic systems: food, logistics, financial infrastructure.

And in Europe, firms like Elaia, Redrice Ventures, and OSS Ventures show a level of specialization that would have been rare just a few years ago.

What ties all of this together is simple:

Venture is no longer trying to be global first.

It’s becoming locally intelligent and globally connected.

And then there’s AI.

But not in the way it’s usually talked about.

AI isn’t a category in this list. It’s the baseline.

You see it embedded everywhere — in Presight x Shorooq backing applied AI at infrastructure level, in Layer Global focusing on AI-driven hypergrowth, in Quantonation pushing into quantum and post-AI physics, in IIT Madras Deeptech Fund bridging research and commercialization.

The interesting part is not that these funds invest in AI.

It’s that they assume everything will be AI-enabled.

Which means the real differentiation shifts elsewhere — into distribution, into domain expertise, into execution.

What’s perhaps most encouraging in all of this is what’s happening at the early stage.

For a while, the narrative was that early-stage investing was drying up — that capital was concentrating into mega-funds and late-stage bets.

But that’s not what this list shows.

Funds like Antler, Also Capital, SNAK Venture Partners, Vest Ventures, and Homegrown Capital are actively operating at the earliest layers — company formation, pre-seed, first checks.

The difference is how they’re doing it.

There’s more discipline. More technical focus. More involvement. Less noise.

It feels less like a race to deploy capital and more like a craft.

If you step back, what February 2026 really represents is not a rebound — it’s a reset.

The venture model hasn’t snapped back to what it was. It’s evolved into something more nuanced:

- More specialized

- More strategic

- More geographically aware

- More aligned with real-world systems

And importantly — more intentional.

83 funds in 28 days is not just activity.

It’s confidence returning — but in a different form.

Not louder. Smarter.

And like every cycle, the most interesting part isn’t which of these funds will succeed.

It’s which of them are early to something everyone else will only understand later.

Because that’s always how venture works.