25 New VC Firms You Should Know About in 2025

There's a number buried in the VCA Annual Report 2025 that should make every LP nervous: 574. That's how many VC firms became zombie funds this year - a 50% jump from 2024. They're not dead. They still have offices, websites, LinkedIn profiles. But they can't exit, so they can't distribute, so they can't raise again. They're just... frozen.

The same report shows that active funds - those that actually deployed capital in the last two years - fell to just 52.7% of the total. Nearly half the VC industry is running on fumes.

So when you look at 25 funds launched between 2022 and 2025, the first question isn't which ones are interesting. It's which ones were built for the market that actually exists now, not the one from 2021.

The Market New Funds Are Walking Into

The macro picture matters before anything else. Global VC funding hit $425-500B in 2025, but deal volume dropped 32%. That's not growth - that's concentration. A few data points that tell the real story:

- 5 companies absorbed 20% of all venture capital deployed globally

- AI captured nearly 50% of total investment; strip out the top 10-20 GenAI mega-deals and the rest of the market is flat to negative

- First-time fund launches fell 35% year-over-year - a decade low; only 68 debut funds raised in the U.S. in the first three quarters of 2025

- Median time to close a fund is now approaching 15 months; some are taking over 17

- Family office VC allocations dropped 64% in H1 2025, from $70.1M to $25.5M - they'd rather hold bonds than lock capital for a decade in funds that may never return it

LPs have consolidated around proven managers and are demanding DPI - actual cash returns, not paper marks. This is the environment new funds are trying to raise in. The middle is hollowing out, and the funds that don't have a structural reason to exist are becoming the next wave of zombies.

The Operator Wave Isn't a Coincidence

A striking number of the new funds in this year's list are led by people who built something real before they wrote a single check. This isn't accidental - it's a direct response to a market where differentiated structures and focused strategies are no longer nice-to-have.

A few that embody this clearly:

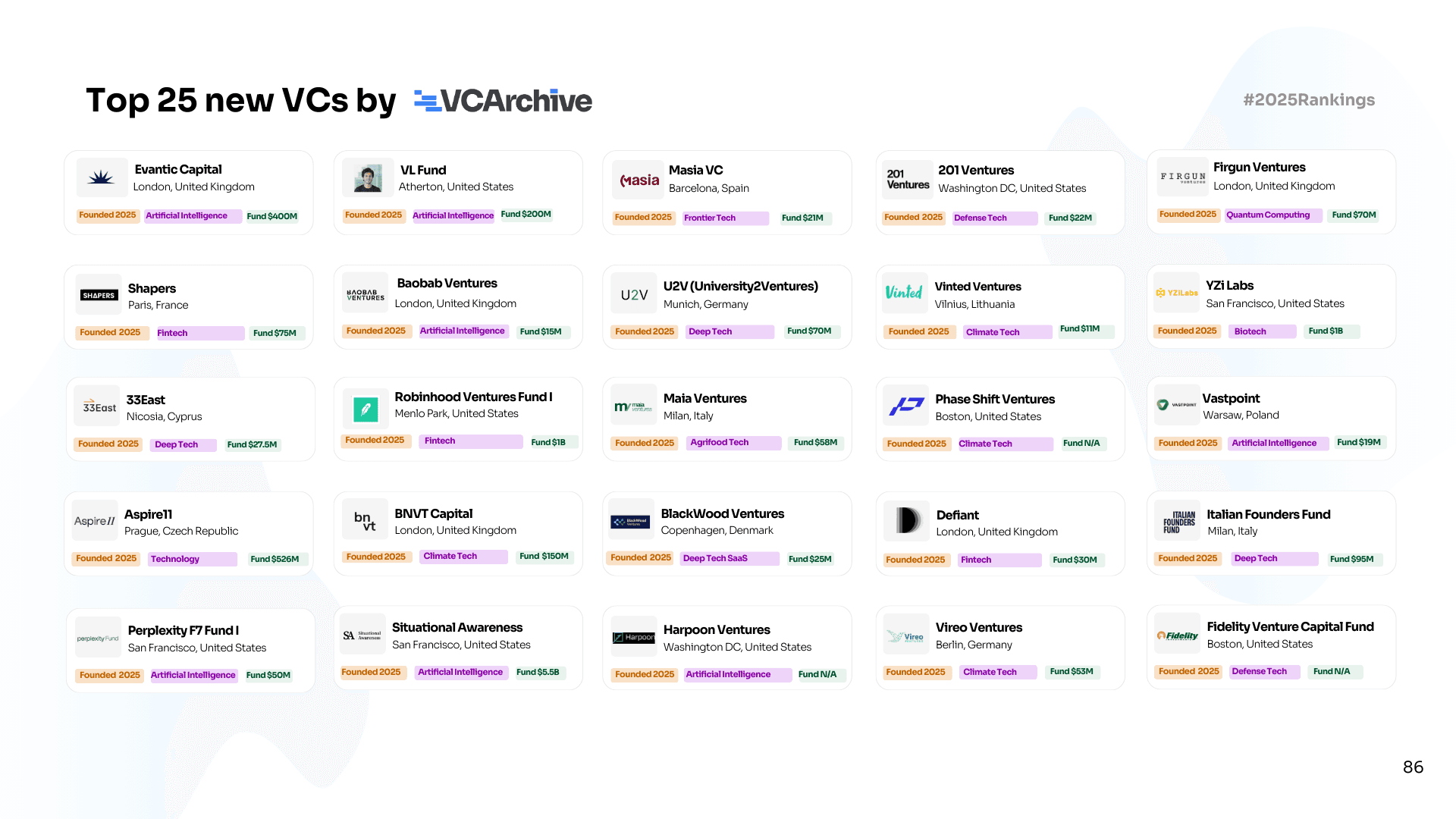

- Evantic Capital (London, $400M) was founded by Matt Miller, who spent 12 years at Sequoia building its entire European strategy and led investments in Graphcore, Confluent, and n8n. He raised $400M by September 2025 - one of the largest solo-GP fund closes in European history - because LPs backed the person, not just the pitch

- VL Fund (San Francisco, $200M) is Victor Lazarte's debut fund, oversubscribed despite the slowest U.S. debut fund market in a decade. Lazarte co-founded Wildlife Studios (largest mobile games company in Latin America) and led Series A rounds for Mercor, Decart, and HeyGen at Benchmark. The track record spoke before the deck did

- Baobab Ventures (London, $15M) is a solo GP fund whose angel track record includes an early bet on ElevenLabs (now $6.6B, roughly 400x return) and an angel position in Revolut - Europe's most valuable fintech. The fund is small precisely because it doesn't need to be large to have conviction

- Phase Shift Ventures (Boston, $28M) backs hard tech founders from inside the MIT and DARPA-adjacent ecosystem, with managing partners who have personally built inside deep tech companies - not just studied them

You can't fake 12 years of knowing every European founder worth knowing. You can't fake a 400x angel return. In a market where generalist platforms are stalling, that's exactly the kind of signal LPs are now paying attention to.

Europe Is the Real Story This Year

The VCA report shows North America controls 52.3% of global VC funds - but the growth story is elsewhere. European VC has been outperforming North America on net IRR over 10 and 15-year horizons - 20.5% vs. 18.0%. European dry powder sits at $54.5B and improving.

What's striking about this year's new fund list is just how European it is - and how specific the geographic theses have become:

- 33East (Cyprus, $28M) is the first institutional VC fund in Cyprus, backed by the EIF and Cyprus government. Being first in an underserved market isn't a weakness - it's a structural advantage that no subsequent fund can replicate

- Italian Founders Fund (Milan, $97M) targets a market that is systematically underserved by institutional seed capital despite producing real companies. Italy is now the fastest-growing VC market in the EU, having tripled total invested capital in five years

- BlackWood Ventures (Copenhagen, $25M) operates in the Nordics - a region the VCA report describes as one of the most talent-dense globally after San Francisco - having produced Zendesk, Trustpilot, Pleo, and Lovable

- Vireo Ventures (Berlin, $54M) focuses specifically on electrification and energy transition in Germany - the largest industrial economy in Europe with binding decarbonization mandates that create structural demand regardless of market sentiment

- Vastpoint Ventures (Warsaw, $22M) bets on Central and Eastern Europe's engineering talent base, backed by PFR Ventures. Poland has produced Booksy, Brainly, DocPlanner, and Packhelp - all from an ecosystem that most Western European funds still treat as a footnote

- Aspire11 (Prague, $540M) is structurally the most significant: the first time Czech pension capital flows into VC at institutional scale, with Partners Group as anchor. Pension capital entering a new market is a multi-decade story, not a single fund

These aren't funds that ended up in their geographies by default. They chose them because they saw the pricing arbitrage - and in some cases the structural first-mover advantage - that larger funds are simply unable to capture.

The Thesis That Surprised Everyone: Defense

One of the most striking patterns in this year's new fund list isn't AI or climate. It's defense.

European defense tech raised $5.2B in 2024 - a 24% jump from 2023, and for the first time surpassing AI funding in Europe. The geopolitical reality driving this isn't going away. And a cohort of new funds are positioning specifically at this intersection:

- 201 Ventures (Washington DC, $22M) is led by Eric Slesinger, a former CIA officer who developed technology for intelligence missions. The sourcing and diligence edge that background provides in defense and dual-use technology is something no traditional VC can manufacture

- Harpoon (Washington DC, $100M) invests in dual-use technologies across defense, AI, and cybersecurity from a team with national security and DARPA backgrounds. The Washington DC base provides natural access to government customers and procurement networks that coastal VCs spend years trying to cultivate

- Firgun Ventures (London, $250M) is the world's first dedicated quantum computing fund, backed by the Qatar Investment Authority, with an advisory council spanning Cambridge, Oxford, MIT, Google, and the EIB. The founders have been angel investors in quantum since 2016 - including an early position in Cambridge Quantum Computing, now Quantinuum

The defense and deep tech thesis is credible precisely because it's genuinely hard to enter. You can't launch a defense tech fund without the right relationships, clearances, and domain knowledge. That's exactly what makes it defensible.

The AI Question: Moat vs. Label

The report is clear: AI captured nearly 50% of all global capital in 2025. Early-stage AI valuations expanded 45% from 2023 to 2025. AI now commands a 25-30% valuation premium over SaaS.

But the report is equally clear on the risk: generic AI wrappers face commoditization and cost pressure. Durable value is going to infrastructure and defensible vertical leaders.

The new funds that understand this are using AI structurally, not decoratively:

- Perplexity F7 Fund I (San Francisco, $50M) has a sourcing moat no other fund on this list can claim: Perplexity's 80,000-developer API network lets the fund see which founders are building the most innovative AI tools before they publicly raise. That's not a thesis - that's a structural information advantage

- Situational Awareness ($1.5B) is the most unusual entry in any new VC list this year. Leopold Aschenbrenner - a 23-year-old ex-OpenAI researcher who graduated valedictorian from Columbia at 19 - raised $1.5B with zero prior professional investing experience and delivered 47% returns in H1 2025 against 6% for the S&P 500. His backers include Patrick and John Collison, Nat Friedman, and Daniel Gross. The strategy is concentrated and high-conviction: long AI infrastructure equities, short industries AI will disrupt, direct positions in frontier AI companies

- YZi Labs (San Francisco, $10B+ AUM) is the rebrand of Binance Labs as an independent entity. The 7-year track record, 300+ portfolio companies, and CZ Zhao's return to active mentorship make it structurally new - not just a name change

The Genuinely New Structures

Beyond thesis, some of the most interesting entries on this list are experimenting with fund structure itself:

The fund structure question matters more than it used to. In a market where DPI is the governing metric and holding periods have stretched to 12.3 years, the way a fund is structured - its LP base, its liquidity mechanics, its fee model - is part of the thesis itself.

The Bottom Line

A "top 25 new VCs" list feels inadequate in a market where 574 firms are effectively dead and the survivors are the ones who found genuine structural advantages - in domain, geography, operator background, or fund structure. The useful question for any founder or LP isn't whether a fund made the list. It's:

What is the specific, defensible reason this team should be writing checks in this market - and does their track record or structure already show signs of it?

The VCA Annual Report 2025 documents a market that has finished being generous. The funds worth paying attention to are the ones that were built knowing that.

Full profiles of all 25 new VCs - fund size, check sizes, portfolio companies, investment thesis, and direct contact details - are available at venturecapitalarchive.com.

Research and curation by the Venture Capital Archive team. Data sourced from the Venture Capital Archive's Annual Report 2025. All information verified as of 2025.

25 New VC Firms You Should Know About in 2025

Rows per page