The LP Content Playbook for VC Firms

Most VC firms create content for founders. Founder advice, market maps, portfolio announcements, podcast interviews, thesis pieces. That content matters, and it is also table stakes at this point.

But there is a second audience that almost nobody writes for, and it happens to be the audience that decides whether your fund exists in three years: limited partners.

The numbers explain why this matters more now than it ever has. The top 30 venture funds captured 75% of all capital raised in 2024, and just nine firms took 46% of it. For funds managing between $100M and $250M, the median number of LPs dropped from 83 in 2022 to 47 in 2024. Median time to close a fund stretched past 15 months in 2025, and first-time managers routinely spend 18 to 24 months raising.

At the same time, the small end of the market is actually moving. In the first half of 2026, almost 90% of LP commitments tracked by Decile Group went to funds under $15M, mostly seed-stage funds with a specialized sector focus. LP money is flowing to exactly the kind of fund most emerging managers are raising. The problem is that there are thousands of them, and LPs cannot tell most of them apart.

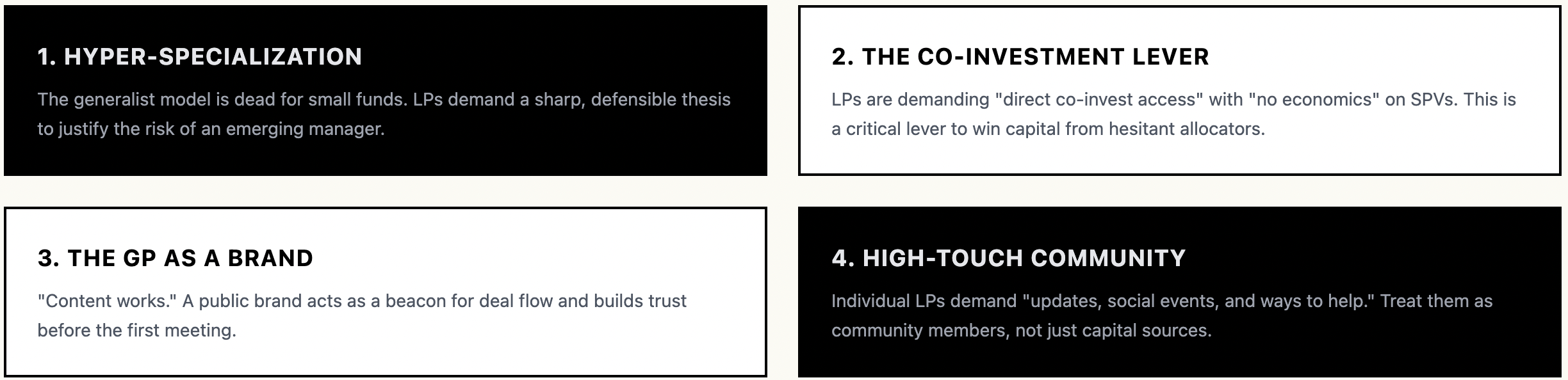

This is where content does real work. A 2025 survey of GPs at 30 small firms found the same things repeated across responses: content works, a strong online brand works, individual LPs want to feel engaged through updates and public presence, and the generalist pitch is dead because LPs now demand a sharp, defensible thesis before they will even take a meeting. LPs also increasingly practice reverse inquiry, meaning they find managers through their public footprint before any introduction happens.

LPs are not just underwriting your returns. They are underwriting your judgment, your access, your discipline, and your ability to see things before they become obvious. Content is the only way to make those qualities visible before a fundraising conversation starts, and most funds are not even trying.

LPs do not need more thought leadership

Here is the mistake I see constantly: a GP decides to "build their brand," and what comes out is founder advice. How to nail your seed pitch. Five mistakes first-time founders make. That content might grow your dealflow, but to an LP it is noise, because every other GP on LinkedIn is publishing the same thing.

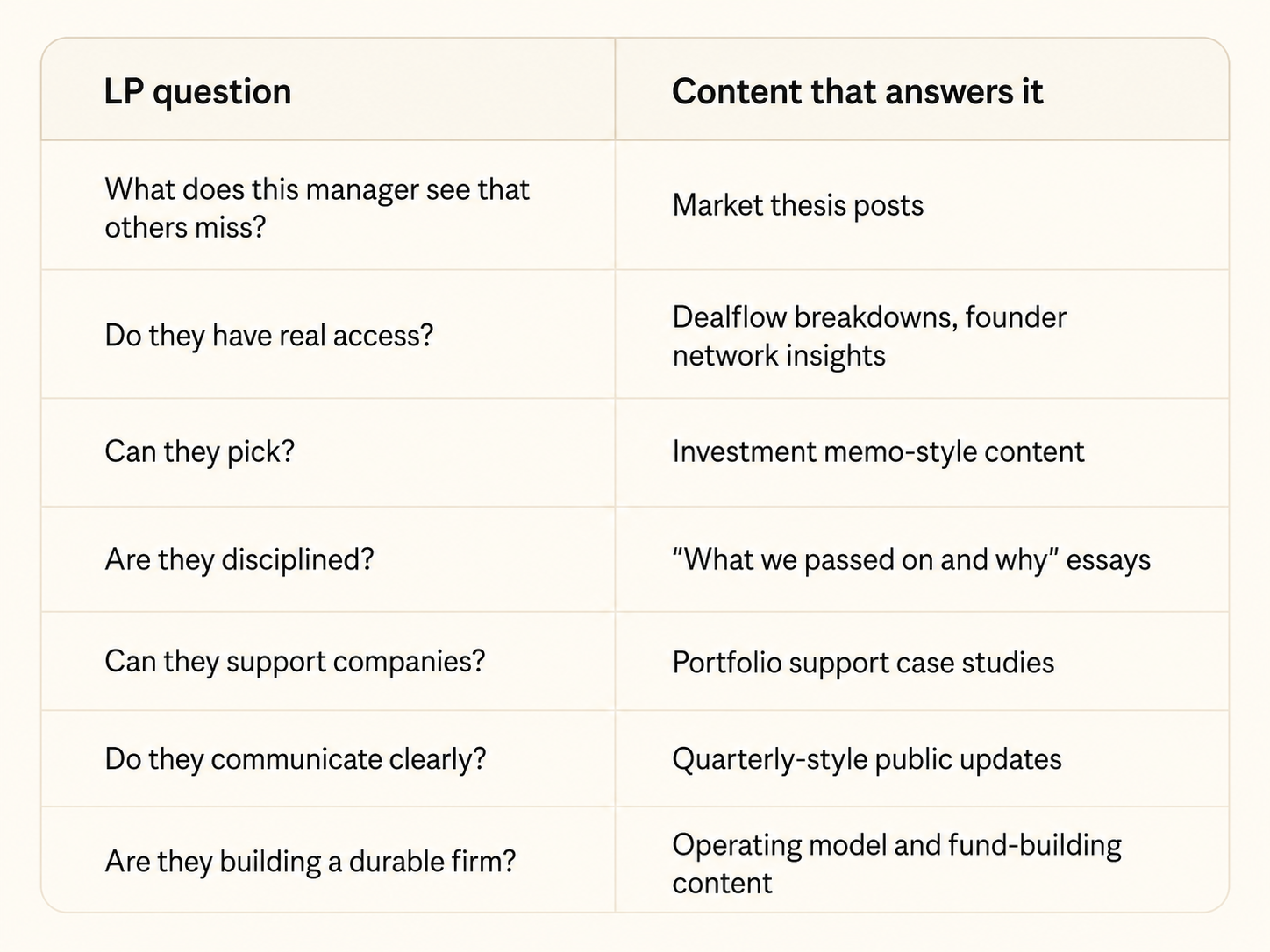

LP-facing content should answer the questions LPs are already asking each other in private. Every piece you publish should map to one of these:

If a piece of content does not answer one of these questions, it might still be useful for founders, but it is not doing anything for your next fund.

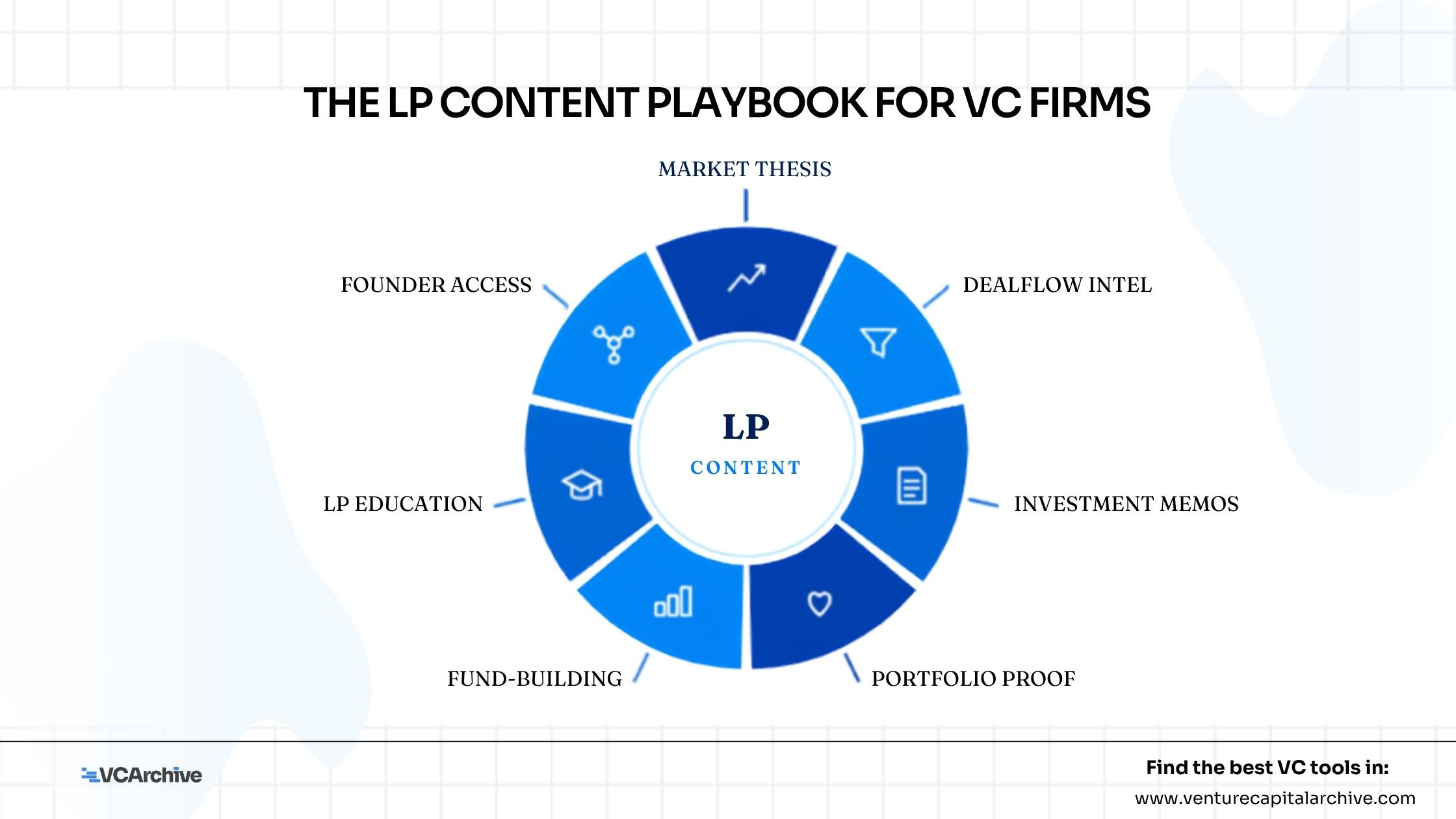

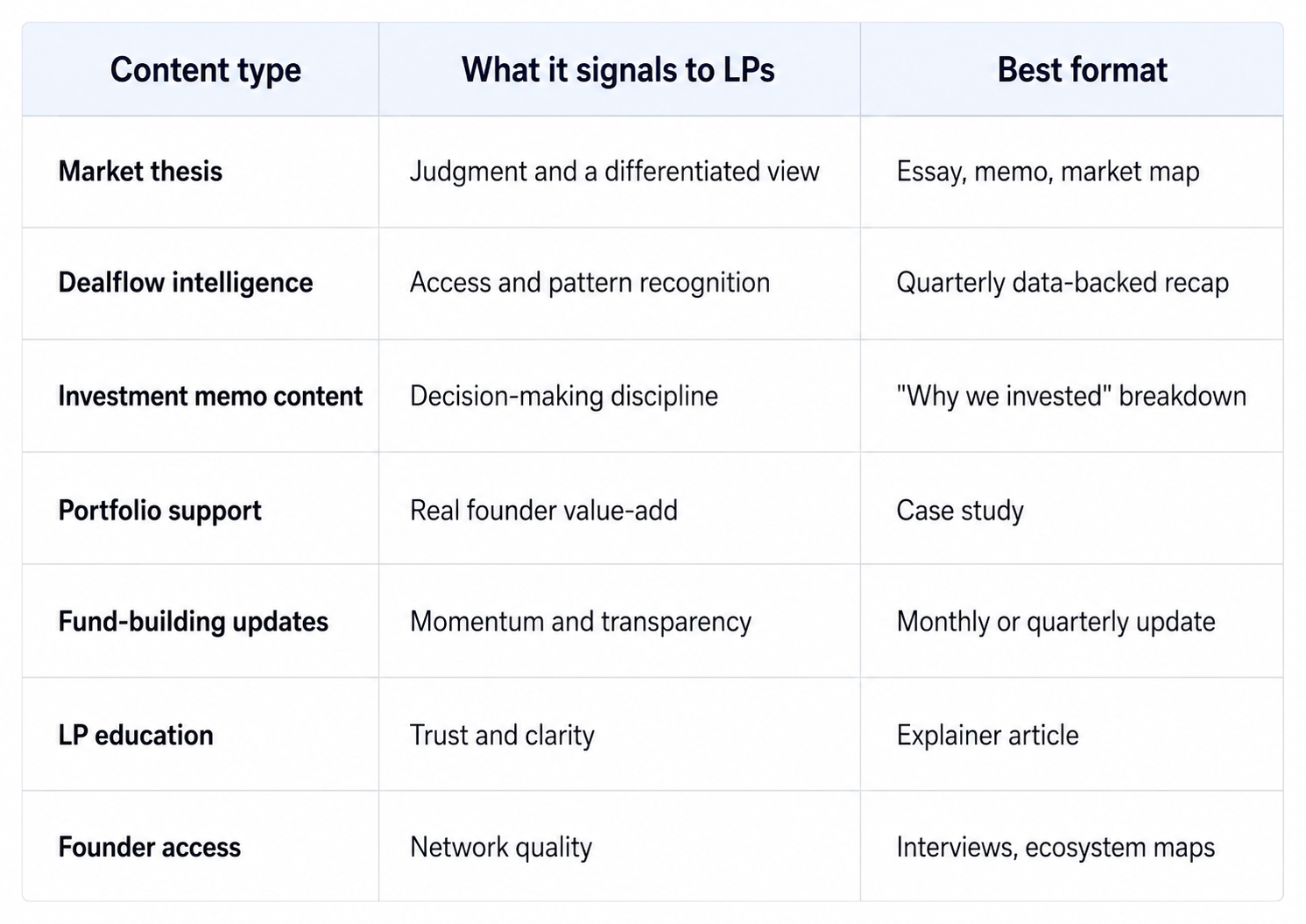

The 7 types of content VC firms should create for LPs

1. Market thesis content

Not "AI is big." LPs have read that take four hundred times this year.

More like: "Why vertical AI is moving from workflow automation to outcome ownership." Or: "Why European defense tech is entering a new institutional phase." LPs want to know how you see markets before consensus forms, because that is literally what they are paying you 2 and 20 for.

Formats that work: sector memos, market maps, "what we believe" essays, "where we are looking right now" posts, and contrarian pieces where you take a real position. The test for whether your thesis content is any good: could a competing fund publish the same piece? If yes, delete it.

2. Dealflow intelligence

This is the highest-leverage format for emerging managers, and almost nobody uses it.

You see hundreds of pitches a year. That aggregate view is something LPs cannot get anywhere else, and it costs you nothing confidential to share. Posts like "What we saw across 200 pre-seed pitches this quarter," "the most common AI infrastructure patterns hitting our inbox," or "where founders are still underbuilding in fintech" prove you are close to the market without revealing a single deal.

LP David Zhou has a useful phrase for what allocators screen for: the difference between access theater and real access. A GP who can describe the texture of their dealflow in specific, current detail is demonstrating real access. A GP who says "we see everything through our network" is performing it.

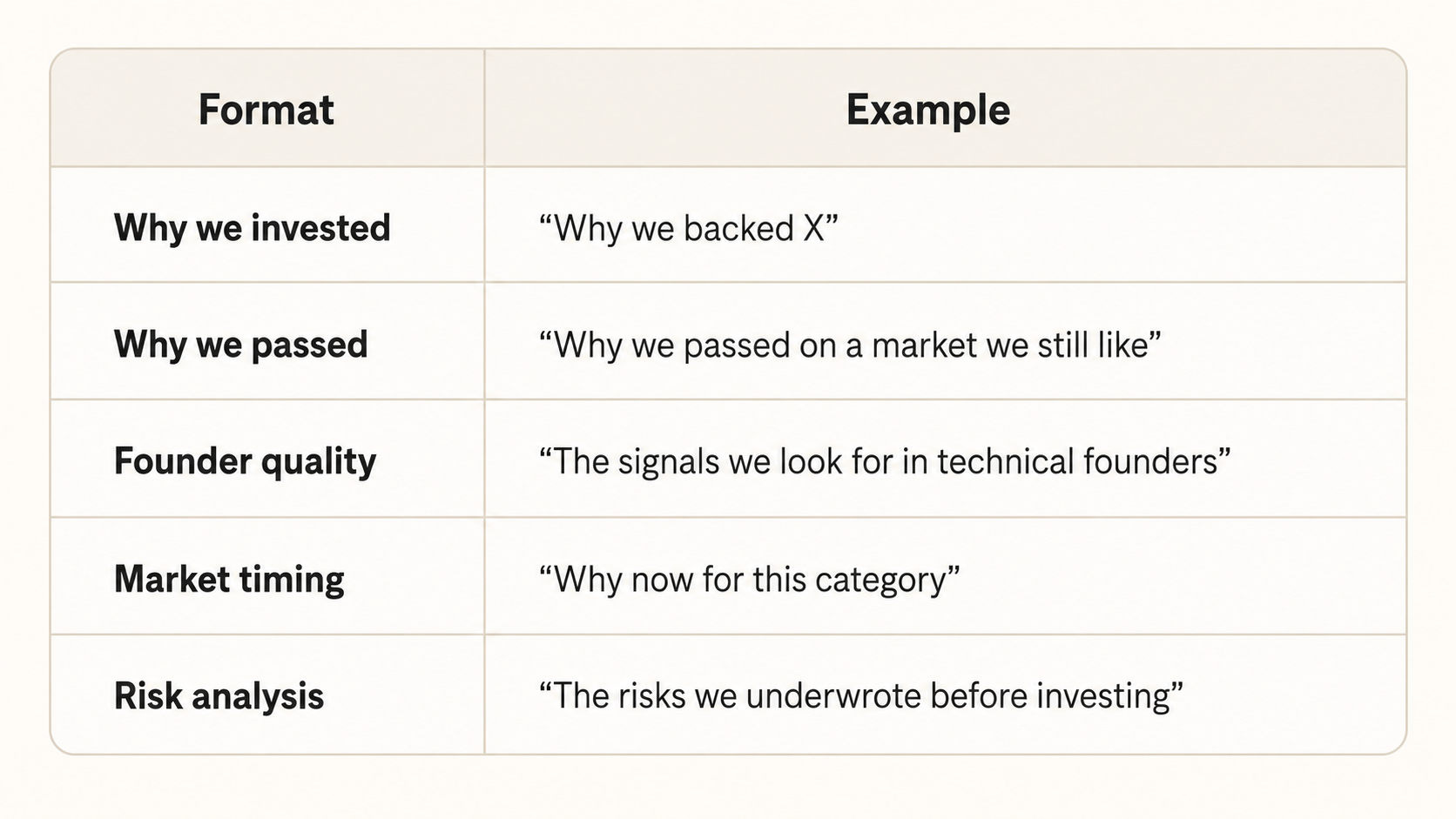

3. Investment memo-style content

This is the closest thing to letting an LP sit inside your head, which is exactly what they want before wiring you money.

Bessemer set the standard here years ago by publishing its actual memos for Shopify, Twilio, Twitch, and Pinterest. You do not need their track record to use the format. Public versions of your thinking work at any fund size:

One honest caveat on the "why we passed" format, because GPs always raise it: yes, there is signaling risk if you name companies. So don't. Write about the market or the pattern, not the startup. "Why we passed on three vertical SaaS deals this quarter despite loving the category" gives LPs everything they need about your discipline without burning a founder relationship.

There is also a useful precedent on the other side of the table. The Side Letter, an LP, open-sourced its entire framework for evaluating emerging managers, and noted that almost no allocators share how they build conviction. Transparency about decision-making is rare enough in this industry that it functions as differentiation by itself.

4. Portfolio support content

Every fund deck on earth says "founder-friendly" and "value-add." LPs have developed complete immunity to the claim. What they have not developed immunity to is proof.

Show the actual machinery: how you helped a portfolio company make its first three sales hires, how you ran a positioning sprint before a Series A, which customer intros converted, how you supported a bridge when a round fell apart. Case studies work here because they are falsifiable. An LP can call that founder during references and check, and the fact that you published it tells them you expect the story to hold up.

5. Fund-building updates

This is the "building a fund in public" angle, done like an adult. Not your feelings about the fundraising journey. The concrete stuff: new advisors, a scout program, a new portfolio support system, a new thesis area, lessons from the first 12 months.

The reference point LPs bring to this is the quarterly letter, and the most common failure modes in LP letters are well documented: either a data dump with no narrative, or a narrative with no data. Your public updates should rehearse the version that does both. A GP whose public updates are structured, consistent, and numerate is giving LPs a free preview of what being their investor will feel like for ten years.

The most extreme version of this working is Packy McCormick's Not Boring Capital. He published the actual memo he used to raise Fund I, shared lightly redacted LP updates in his newsletter, and reserved LP allocation for readers. Fund I closed at its $9.9M cap with 133 LPs and deployed in six months, and Fund II raised $30M. You do not need a 100K-subscriber newsletter to copy the underlying move, which is treating the fund's own progress as content that lets future LPs watch you operate before they ever commit.

6. LP education content

This works especially well if you are raising from family offices, operators, founders, and individuals rather than institutions, which describes most sub-$15M funds, which is where 90 percent of LP commitments went in the first half of 2026.

These LPs are often writing their first or second fund check, and nobody has explained the mechanics to them. So explain it: how VC fund economics actually work, what to ask before backing an emerging manager, how co-investment rights work, what TVPI, DPI, and MOIC tell you and what they hide. A GP who can explain fund metrics in plain language is signaling two things at once, that they understand the numbers deeply and that their reporting will not require a translator.

7. Founder access content

The quietest question in every LP's head: can this manager actually get into good deals?

You cannot answer that by claiming it. You answer it by displaying the network in motion: founder interviews, ecosystem maps, founder survey data, "what founders are asking us right now" posts, recaps of the dinners and events you host. For small funds competing on niche access rather than brand, this is the entire game. An LP looking at a fund focused on, say, Israeli cybersecurity or European climate hardware wants visible evidence that the relevant founders already treat you as part of their world.

What not to do

A few things that actively hurt with LP audiences, learned from watching funds do them:

Portfolio announcement spam. A feed that is nothing but "thrilled to announce our investment in" tells an LP nothing about how you think, only that you have a Canva subscription.

Recycled founder advice. It signals you are optimizing for reach, not for the audience that funds you.

Inconsistency. Publishing four pieces in January and nothing until June reads as exactly what it is, a GP who picks up content when fundraising starts and drops it the moment a close happens. LPs notice, because consistency in public is a proxy for consistency in reporting.

Hot takes on other investors or public market calls outside your lane. You are being underwritten on judgment. Spending it on engagement bait is a bad trade.

Where this content should live

For the LP base most emerging managers are actually raising from, family offices, operators, founders who angel invest, and individuals writing their first fund checks, LinkedIn is the primary channel. These people are on it daily, and GP surveys confirm that individual LPs specifically want more engagement, more updates, and more public presence from the managers they back. Institutional allocators are quieter on the platform, but they still look you up before and after every meeting, which means your profile and your last twenty posts function as a pre-read for diligence whether you intend them to or not.

So the job is twofold. LinkedIn is where LPs discover you and form a first impression of how you think, and an owned channel, a newsletter or blog, is where the longer arguments live and get forwarded between LPs.

A practical setup that works for a small fund: one long-form piece a month on the owned channel, cut into several LinkedIn posts across the month, plus one dealflow or fund-building recap per quarter on a schedule you never miss. That is maybe two days of work a month, and it compounds in a way that another founder coffee chat never will.

Making judgment visible

The best firms do not only market to founders. They build trust with the entire ecosystem around the fund, and for LPs, content is not about being loud. It is about making judgment visible.

In a market where nine funds take nearly half the capital and an emerging manager spends two years raising, the GPs who win are creating a public record of how they think, where they have access, and why their fund deserves to exist. Most of your competition is still posting founder advice. That is the opportunity.

Huge shoutout and thanks to Ivelina Divena for writing this awesome guest post for our readers!

Check out Ivelina Divana's LinkedIn profile and EverythingStartups for more.

More from Ivelina Dineva

No other articles from this author yet. Visit their profile.