The Hidden Rule That Separates Top Tier VCs From Everyone Else

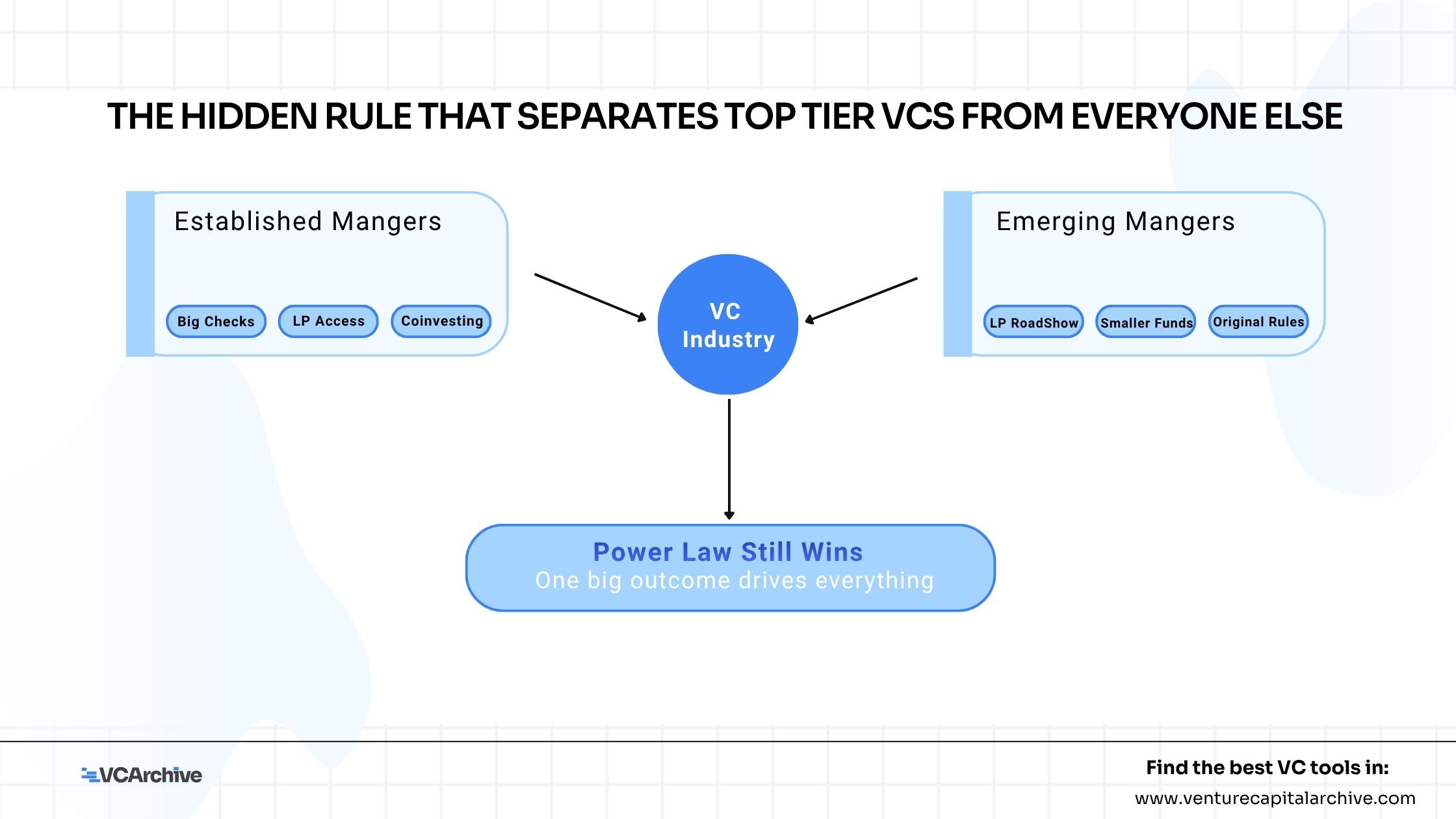

I have spent a long time watching venture capital from the inside. I have seen fund cycles come and go, watched LPs tighten and loosen their grip, and backed founders at every stage. And right now, what I see is something I have not seen quite so clearly before: the industry is splitting into two very different groups.

One group has the capital, the brand, and the access to operate in a new way. The other group, the true emerging managers, is still working with the original rules. And here is what I want to say clearly: those original rules still work. They just take more discipline and more patience to execute today.

The Split I Am Seeing

The managers with full access

On one side are the managers who have already made it to a certain level. They have strong LP relationships, they see deals early, and they can write big checks into rounds that were not even possible a few years ago. For them, venture today feels like a different game. They are co-investing alongside sovereign wealth funds, moving into AI infrastructure, and building structures that would have seemed unusual not long ago.

Access compounds. Once you are in the room, it becomes easier to stay in the room. That is what I observe with this group.

The emerging managers still grinding

On the other side are the first- and second-time fund managers. People with real conviction and real expertise, but without the institutional weight of their larger peers. They are still doing the full LP roadshow. They are competing for deals against funds ten times their size. They are building everything from scratch.

What I want to be clear about is this: they are not playing a broken game. They are playing the original game. The one that produced many of the best returns in the history of this asset class. It is just harder right now, and it requires more focus.

The Old Way Still Works

I have watched too many emerging managers panic when they see the headlines. Mega-rounds, billion-dollar AI bets, funds raising on reputation alone. It can feel like the rules have changed completely.

But the basics have not changed. Building real relationships with founders before they raise still works. Investing in sectors you genuinely understand still works. Being quick and direct in a way that big funds cannot still work. Taking a concentrated position in your best ideas rather than spreading thin still works.

What has changed is the pace. LP decisions take longer. The bar for a track record is higher. Patience, which was always important in this business, is now a requirement.

Discipline is your edge

For emerging managers, being disciplined is not a limitation. It is the advantage. A smaller fund that deploys capital carefully, manages reserves well, and does not chase hot deals it cannot win is not playing small. It is playing smart. The managers I have seen survive and grow are the ones who stopped trying to compete on terms they could not beat, and instead focused on what they actually had: speed, genuine access to founders, and real expertise in their space.

Some Managers Can Play Both Sides

There is a middle group worth talking about. These are managers, usually running funds in the $150M to $400M range, who have built enough credibility to access some of the newer opportunities while still keeping the flexibility of a smaller shop. They can write a meaningful Series A check and still have the reserves to follow on at Series B.

This is where many ambitious emerging managers want to end up. Getting there does not just require returns. It requires a reputation that is built slowly, through consistent judgment over many years. The old playbook is exactly what gets you there.

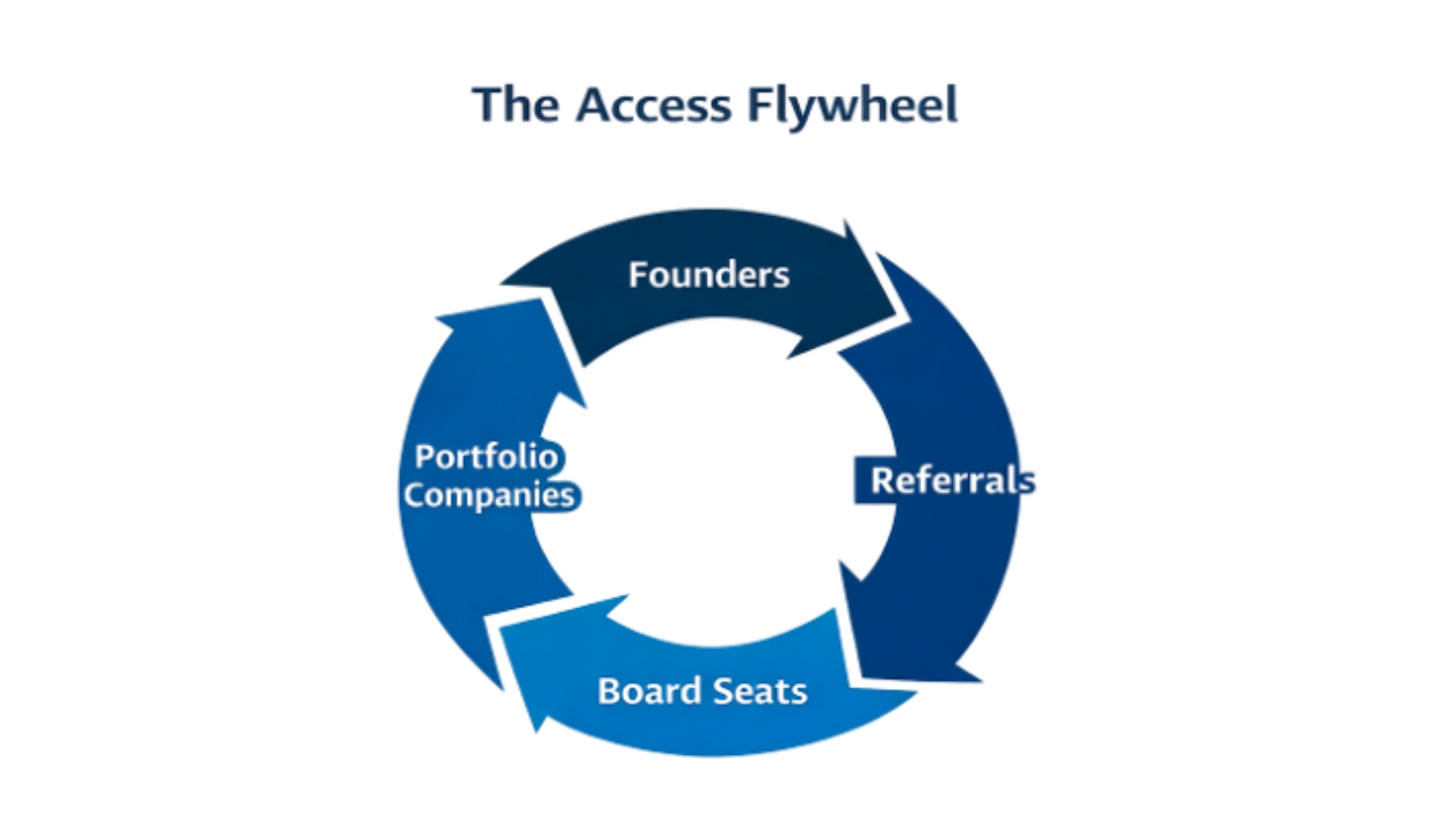

What access actually means

When I say access, I do not mean knowing the right people at dinner parties. I mean structural position in the ecosystem. It means founders call you before they decide to raise. It means your portfolio companies introduce you to other founders naturally. It means sitting on boards that give you real information, not just updates in a deck.

That kind of access takes time to build and it is not linear. One great outcome, one company that really breaks through, can do more for your position than years of steady but quiet returns. Which brings me to the thing that has never changed.

The Math of Venture Has Not Move

“You still need that one big outcome to drive your returns. And if you find it, the rest of the portfolio tends to take care of itself.”

Every LP knows this. Every GP believes it. And yet it is easy to lose sight of it when you are deep in portfolio management mode. Venture capital is a power law business. The top funds are not the ones that bat the highest average. They are the ones that found the outlier.

Own more, not just earlier

If your fund returns are driven by one or two outcomes, then how much of those outcomes you own matters enormously. A fund that gets into a great company early with real ownership will outperform a fund that gets in later with a small slice, even if the entry price looks more comfortable. Chasing a deal just to be in the cap table, and giving up ownership to get there, is one of the most common mistakes I see from emerging managers.

Reserves are not a backup plan

If your best company is not obvious at Series A, you need to be able to follow on when it becomes obvious at Series B or C. Managers who run out of follow-on capital end up watching their best bets get diluted while they sit on the sidelines. Reserve strategy is not a treasury decision. It is a return decision.

More companies does not mean less risk

There is a belief, more common among newer managers, that spreading across 40 or 50 companies lowers risk in a useful way. It does not. If none of those companies has the potential to return the whole fund on its own, diversification is just noise. Conviction and concentration, sized carefully, is almost always the better path. The math of venture demands it.

Where I Think This Is All Going

The split I described at the start is not going away soon. If anything, it will get more defined. Capital will keep concentrating at the top, and the entry level will keep getting more crowded. That is the reality.

But I do not think this is bad news for emerging managers who are willing to stay focused. The original approach, doing the work, knowing your space, building real founder trust, and staying disciplined on ownership and reserves, is still a viable path to building a great fund.

The managers who will define the next decade of venture are probably not trying to replicate what worked in the last one. They are more specialized. They are closer to their founders. They are more honest with their LPs about what they are building and why.

And somewhere in one of their portfolios, there is a company nobody expected. A bet that looked small at first, and then did not. That company is going to tell the whole story.

That is still how this business works. And I do not think it is going to change.

Huge shoutout and thanks to Trace Cohen for writing this awesome guest post for our readers!

Check out his LinkedIn profile and Six Point Ventures for more.

More from Trace Cohen

No other articles from this author yet. Visit their profile.