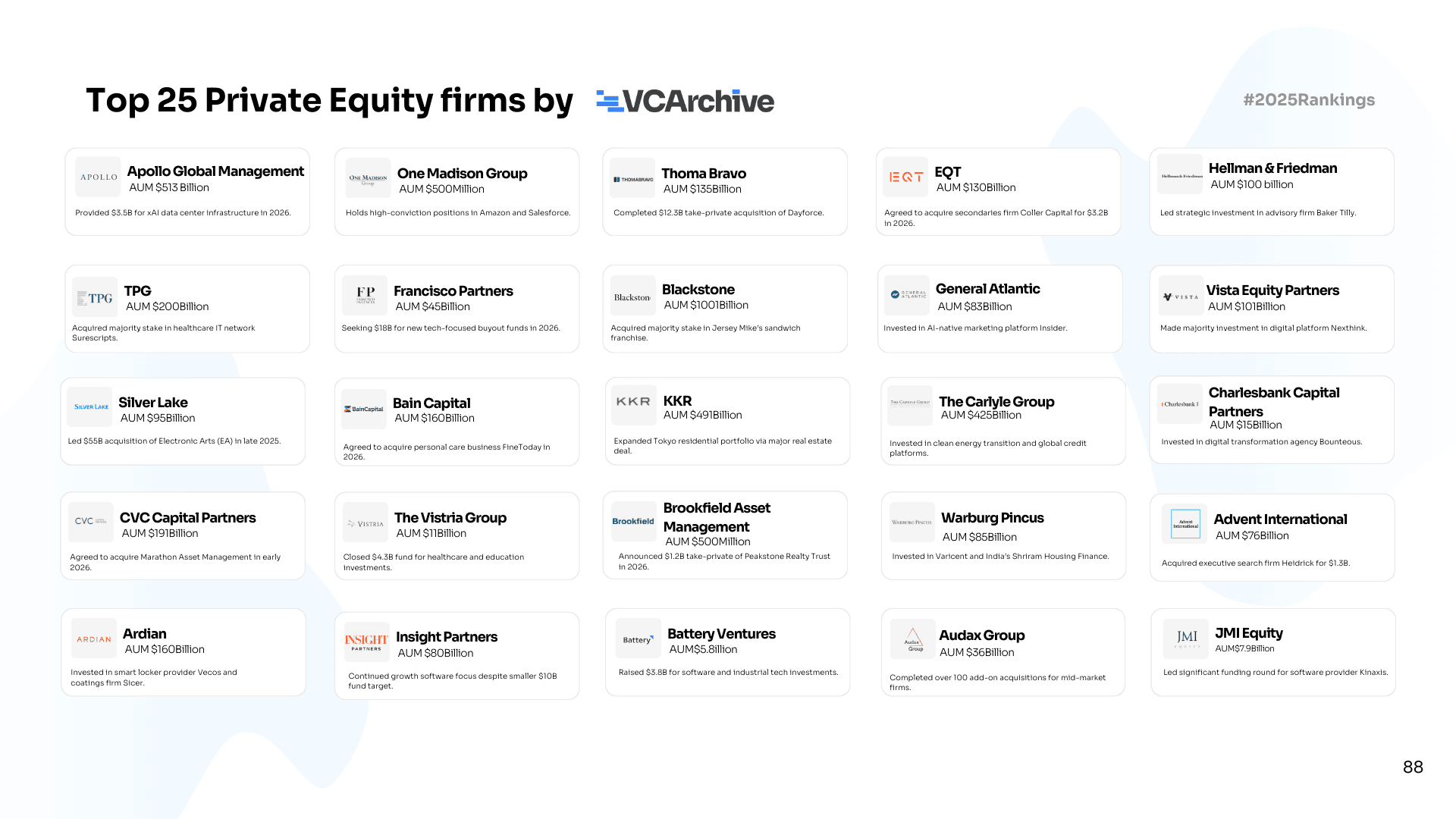

The 25 Private Equity Firms That Moved Markets in 2025

Venture capital gets the profiles, the podcasts, the Twitter threads. Private equity gets the assets. In 2025, alternative assets under management hit $17.3 trillion globally, heading to $21 trillion by 2027. Private equity is the largest slice. The 25 firms on this list manage more than $4.5 trillion between them.

One of them just crossed $1 trillion alone.

The number that should reframe how you think about this

574 VC firms became zombies in 2025. Meanwhile, Apollo grew its fee-related earnings at 20% CAGR from 2020-2025. The difference isn't talent or timing, it's structure. Apollo has 63% permanent capital, meaning the majority of its assets never need to be returned to investors. No fund cycles. No LP pressure. No forced exits at the wrong time. That is a structural moat that no VC fund however well-branded can replicate.

This is the part of the market most people in venture don't spend enough time understanding.

Who's actually on this list and why the range is absurd

- Trillion-dollar platforms: Blackstone ($1T+), KKR ($491B), Apollo ($513B), Carlyle ($425B), Brookfield ($500B)Multi-asset machines - PE is just one lever among credit, infrastructure, real estate, insurance

- Software specialists: Thoma Bravo ($135B), Vista Equity ($101B), Silver Lake ($95B), Francisco Partners ($45B) - Buy profitable software companies, take them private, optimize, re-exit

- Growth equity: General Atlantic ($83B), Warburg Pincus ($85B), Hellman & Friedman ($80B), Advent ($76B) - Back proven businesses scaling internationally or transitioning ownership

- Mid-market builders: Audax ($36B), Charlesbank ($15B), JMI Equity ($7.9B), Vistria ($11B) - Smaller platforms, tighter focus, often sector-specific conviction plays The gap between Blackstone and One Madison Group ($500M) on this list is 2,000x. Both are technically "private equity." They are not playing the same game.

Three things PE got right in 2025 that VC got wrong

Exits. The IPO freeze that paralysed venture for three years barely dented PE. Why? Because PE has never been dependent on public markets; trade sales, secondary buyouts, carve-outs, and recapitalisations all work just as well.

When the secondary market hit $240 billion in 2025, that was largely a PE story. EQT's $3.2B acquisition of secondaries firm Coller Capital was a deliberate bet that secondary infrastructure will be a core competency for decades.

AI as a tool, not a thesis. Every VC fund in 2025 claims to be an "AI investor." Most PE firms quietly embedded AI into their operations, cutting due diligence cycles by 30-50%, building proprietary sourcing data stacks, running portfolio monitoring at scale without ever putting it in a press release.

The VCA report is explicit: very few buyout funds view AI as a standalone investment theme. They're using it to move faster and price better. That compounds quietly.

Permanent capital. While VC funds are scrambling to show DPI to anxious LPs, Apollo is sitting on 63% permanent capital. Carlyle and Ares posted the strongest 5-year AUM growth rates among major managers. The firms that built structures where capital doesn't need to be returned have an operating cadence that looks nothing like the 10-year fund model everyone else is trapped in.

The software PE story deserves its own paragraph

Thoma Bravo's $12.3B take-private of Dayforce in 2025. Vista Equity backing Ping Identity, Gainsight, Mediaocean. Francisco Partners owning Payoneer, Forcepoint, NMI. This cohort figured out something the broader market underpriced for years: software businesses are the ideal buyout targets. High margins. Recurring revenue. Asset-light. No factories to run, no inventory to manage, no commodity exposure. You buy the company, run the operational playbook, and re-exit at a premium sometimes to another PE firm, sometimes to a strategic, sometimes back to public markets.

The VCA report confirms buyout investors in 2025 are focused almost exclusively on cash flow and operational discipline. Software delivers both on day one. That's why this cohort is writing the biggest checks in PE right now.

What 80% of LPs just voted for

The Adams Street Global Investor Survey tracked in the VCA report found:

- Over 80% of institutional investors plan to maintain or increase private market allocations in 2025

- 88% plan to expand co-investment allocations targeting up to 20% of their total private markets portfolio in direct and co-investment vehicles

- Technology and healthcare together attracted 47% of planned new commitments

- China exposure fell to just 11% of investor interestm, capital is rotating to North America, Europe, and India

This is the LP behavior that feeds these 25 firms. When pension funds, sovereign wealth, and family offices collectively decide to put more into private markets, the firms with the longest track records and largest platforms absorb the majority of that capital. The rich-get-richer dynamic the VCA report documents in VC is even more pronounced in PE.

The honest part

PE is not built for founders. It is built for returns. The firms on this list are not picking companies they believe in. They are allocating capital to risk-adjusted return profiles across geographies, sectors, and asset classes. Understanding that distinction is the prerequisite for any founder, operator, or LP thinking about engaging with them.

Full profiles - fund numbers, check sizes, sector focus, co-investors, portfolio companies, and direct contacts for all 25 firms at venturecapitalarchive.com.

Research and curation by the Venture Capital Archive team. Data sourced from the VCA Annual Report 2025. All AUM figures as of 2025.