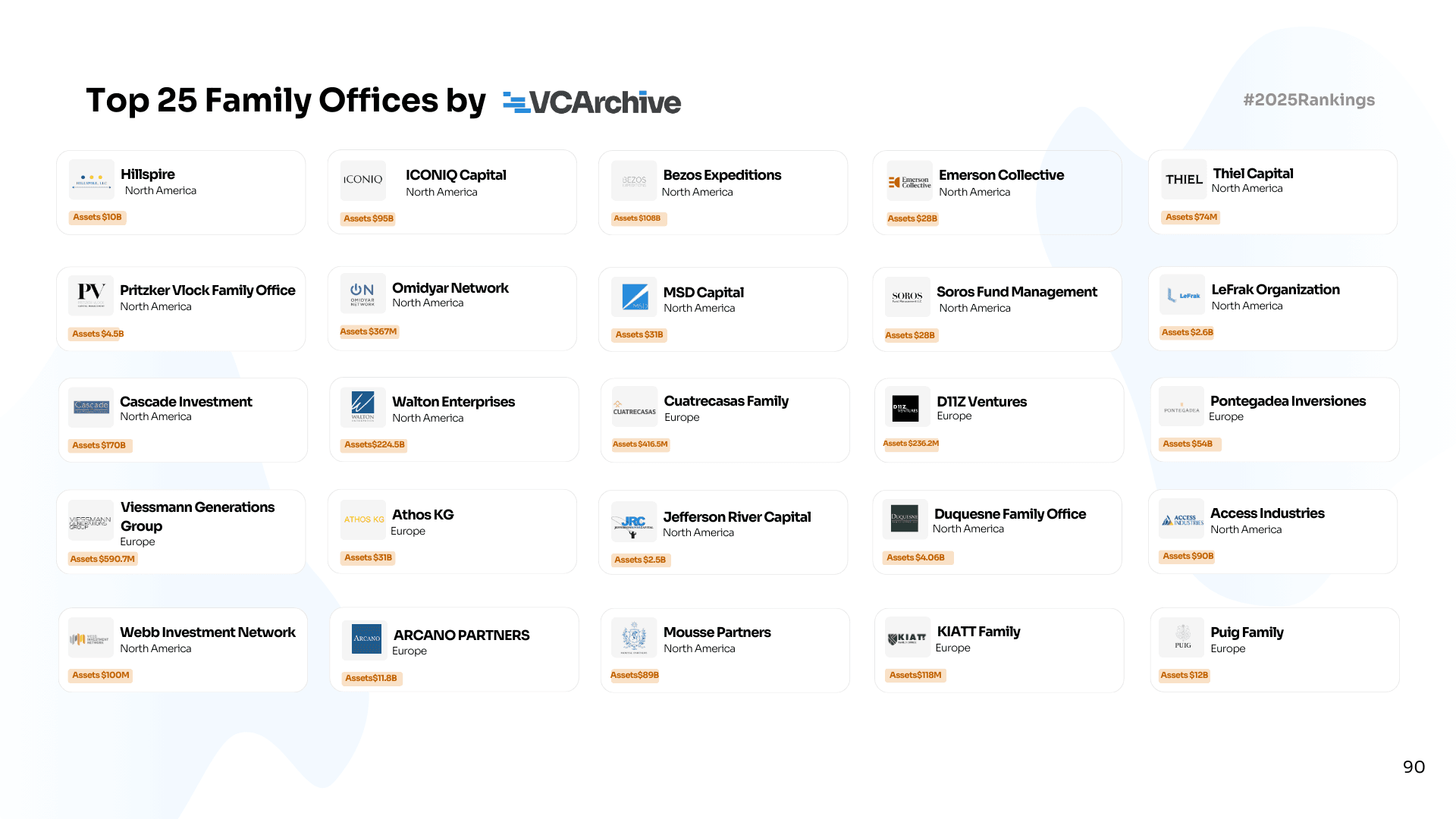

The 25 Family Offices Behind 2025's Biggest Moves

Here is the most counterintuitive finding in the VCA Annual Report 2025: family office VC allocations collapsed 64% in H1 2025 - from $70.1M to $25.5M average per office. They didn't lose money. They didn't panic. They made a deliberate choice. They'd rather hold bonds, public equities, or private debt than lock capital for a decade in a fund that may never return the promised multiple.

And yet - every family office on this list is still actively investing. Just not the way they used to.

This is the distinction the industry keeps missing. Family offices didn't exit investing.

They exited blind trust in intermediaries. When you have $224.5B like Walton Enterprises, or $170B like Cascade Investment, you don't need a fund manager to pick winners for you.

You build the infrastructure to pick them yourself.

What the typology grid above actually shows

Four completely different types of capital operate under the "family office" label. Getting this wrong is the most common mistake founders make when approaching them.

- Generational wealth platforms - Walton, Cascade, Mousse Partners ($89B, the Chanel family office), Access Industries ($90B, Warner Music Group, Spotify, LyondellBasell), Pontegadea ($54B, Amancio Ortega's Inditex fortune deployed into global real estate). These aren't investors the way VCs are investors. They are permanent capital vehicles managing multi-generational wealth. Their time horizon is decades. Their primary mandate is preservation. When they back a company, it's a strategic signal - not a financial bet.

- Frontier and conviction offices - Bezos Expeditions ($108B), Thiel Capital, Hillspire (Eric Schmidt's office), D11Z Ventures (Berlin-based deep tech). These are founder-led and intellectually driven. They don't follow consensus. Bezos Expeditions backed Perplexity AI, Skild, and Grail alongside Blue Origin - not because a fund manager recommended them, but because the principal has a point of view about what matters. Thiel Capital backed Palantir and SpaceX before anyone else thought that was rational. The pattern: high conviction, high concentration, long hold.

- Growth and macro offices - ICONIQ Capital ($95B, managing the wealth of Zuckerberg, Sandberg, and other Silicon Valley founders) is the most institutionalized on this list - it operates more like a growth equity fund than a family office. Soros Fund Management ($28B) and Duquesne ($4.06B) are macro-first, moving across public and private markets based on global thesis, not sector thesis.

- Mission-driven offices - Emerson Collective (Laurene Powell Jobs, $28B, backed Anthropic, Mistral AI, Formation Bio), Omidyar Network (eBay fortune deployed into financial inclusion and civic tech globally), Athos KG (the Thomas and Andreas Strüngmann family office, founding investors in BioNTech long before COVID made it famous). These offices blur the line between philanthropy and investing - and they're often first into categories that only become obvious years later.

Three things from the report that explain exactly what's happening

Family offices are no longer patient with funds that can't distribute. The VCA report documents that 52% of companies from 2021-vintage funds have been stuck without an exit for four years. DPI importance to LPs grew 2.5x in three years. Family offices feel this more acutely than pensions - they have principals with specific liquidity needs, not 30-year mandate horizons. When they say they're moving to bonds, they mean it.

But they're moving money into direct investing, not out of private markets. The Adams Street survey shows 88% of LPs plan to expand co-investment allocations. Family offices are the most active co-investors in the market - ICONIQ co-invests alongside Sequoia and Silver Lake in late-stage tech. Bezos Expeditions joins Lux Capital on frontier science bets. They're getting the deal access without paying 2-and-20 for a generalist to make the call.

Europe is building a serious family office ecosystem, and it looks different. Eight of the 25 offices on this list are European - Athos KG, Pontegadea, Viessmann Generations, D11Z Ventures, Arcano Partners, Puig Family, Cuatrecasas, KIATT. The European offices skew toward industrial heritage (Viessmann made boilers for 100 years before pivoting to climate tech), life sciences (Athos was in BioNTech from the start), and luxury (Puig built Charlotte Tilbury and L'Occitane into global brands). The VCA report notes European AUM growth will lag North America through 2027 - but the quality of European family office capital is maturing fast, and it tends to be more patient and less herd-driven than U.S. equivalents.

What actually makes family office capital worth pursuing

For founders, the honest answer is: it depends entirely on which type you're dealing with.

- Generational wealth platforms write big checks but move slowly and need strategic alignment, not just financial returns

- Frontier offices are accessible if you can get to the principal - but they're high-conviction and will pass fast if you don't fit the worldview

- Growth offices like ICONIQ operate like institutional funds and evaluate you like one - they want traction, metrics, governance

- Mission offices back ideas before markets exist, but they want to see the impact thesis as clearly as the business model

The worst mistake founders make is treating family office capital as easier to raise than VC. It's different, not easier. The diligence is less standardized, which means relationships matter more. The decision process is more opaque, which means warm introductions are almost mandatory. And the hold expectations are longer, which means you need to be aligned on timeline from the start.

Full profiles of all 25 family offices - AUM, ticket sizes, investment thesis, portfolio companies, preferred contact method, and direct contact details - at venturecapitalarchive.com.

Research and curation by the Venture Capital Archive team. Data sourced from the VCA Annual Report 2025 and public disclosures. All AUM figures as of 2025.

The 25 Family Offices Behind 2025's Biggest Moves