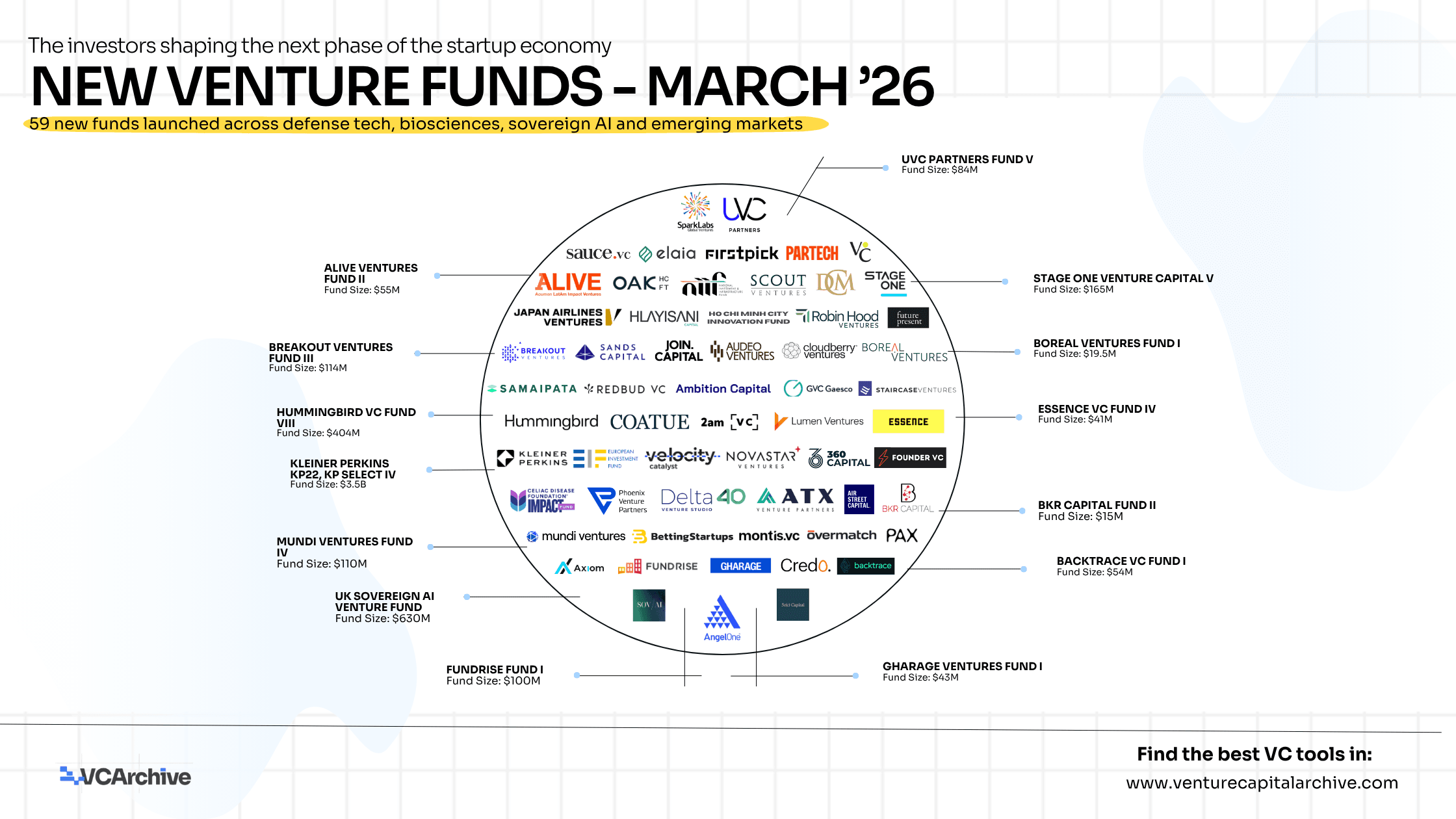

New Venture Funds - March 2026

March didn’t drop any bombshells. No $10 billion monster fund. No dramatic sovereign wealth shake-up. Just 59 new funds quietly launching across 28 countries.

Each one is a very specific bet on a disease, a protocol, an industry, a city, or a slice of tech that some team decided was worth putting their reputation and money behind. Nothing flashy, but if you look closely, the signal is there.

This isn’t a big directory. It’s my attempt to cut through the noise and figure out what this batch of funds actually says about where serious capital is moving right now.

The Market Nobody’s Talking About

VC fundraising is still tough. First-time funds hit a ten-year low in 2025. Small funds (under $250M) keep losing ground to the mega-funds. Holding periods are stretching past 12 years, and a ton of 2021 companies are still stuck with no exit in sight.

Against that backdrop, 59 new funds in one month actually tells you something important. The money isn’t gone. It’s just gotten pickier, more spread out geographically, and way more focused on specific theses.

The real question that matters isn’t who raised the biggest check. It’s which fund has the clearest answer to: why this, why now, and why us?

March’s group gave 59 different answers. A handful are genuinely worth watching.

Geography: The Map Keeps Shifting

MENA venture activity jumped 145% last year. India was up 56%. Europe has been quietly beating North America on long-term returns (20.5% vs 18.0% net IRR over 10 and 15 years) while offering cheaper entry points. LPs are starting to notice that math.

You can see it in March’s cohort. Funds showed up from Vietnam, Colombia, Japan, Lithuania, Israel, South Africa, Italy, Netherlands, Mexico, Canada, you name it. A lot of the interesting ones weren’t in San Francisco, and plenty weren’t even in English-speaking markets.

FIRSTPICK in Vilnius caught my eye. They’re doing pre-seed checks from $50K to $300K into Baltic founders at a pace big institutions can’t touch. The Baltics have already given us Starship Technologies, Bolt, and Wise. The question isn’t if good companies come from there, it’s whether the first real money gets in before London and Berlin swoop in. FIRSTPICK is betting they’re already on the ground.

Same story with the Ho Chi Minh City Innovation Fund - a $191M government-backed vehicle. Vietnam isn’t waiting around for Sequoia scouts anymore. With VNG, FPT, and Vingroup in the mix, they’re building their own capital stack.

Specificity Is the New Moat

What stands out most isn’t size or location. It’s how narrow and clear some of these theses are.

BettingStartups is almost perfect in its clarity. If you’re in iGaming, you know to go to them. If you’re not, you don’t waste your time. That kind of positioning is rare and powerful.

The Celiac Disease Foundation fund is even weirder (in a good way). It’s structured as venture philanthropy, all returns go straight back into the foundation. Only 1% of people with celiac are diagnosed and there’s still zero FDA-approved treatment. Their real advantage isn’t the money. It’s their patient network and relationships with doctors that no normal VC can copy.

Broad “we invest in tech globally” theses are dying. The market wants sharp, specific edges now.

Defense Tech Is Getting Serious

Defense-adjacent investing keeps normalizing. March added three very different takes on national security and tech.

Scout Ventures (Austin, Fund V) has been doing this since 2009. They back frontier tech from founders with military, intelligence, or national lab backgrounds. 62 exits, names like Shield AI and Voyager Space, they have real proof.

Overmatch Ventures is narrower: open source software for national security. Their bet is that the next wave of defense tools will be built on open source by people who already live in those communities.

GHARAGE Ventures in Riyadh sits at the crossroads of defense, AI, and industrial tech in the Gulf. That gives them access to sovereign money and government contracts that Western funds can only dream about.

B2B SaaS: Getting More Focused

Six funds are explicitly chasing early-stage B2B SaaS. Sounds crowded, but they’re not stepping on each other much.

Backtrace VC stands out because one of the GPs is Frederic Kerrest, co-founder and former COO of Okta. When he says “been there, done that,” it actually means something. That operator credibility changes the conversation at pre-seed.

Pax Ventures also looks strong, their portfolio already includes Superhuman, Glean, Modern Treasury, and others. For a first fund, that shows real founder access.

Health & Bioscience: Different Flavors

Breakout Ventures is betting biology is becoming programmable like software, especially where it can replace industrial chemical processes.

Dimension ($700M) keeps doubling down on AI-driven drug discovery and extending healthspan. Solid track record so far.

VitaminºC in Mexico City is doing something more community-driven for Latin America, focused on prevention and expanding access.

And yes, the Celiac fund is still the strangest (and most interesting) one in the bunch.

Government Money Is Getting Bolder

The UK Sovereign AI Venture Fund (£1B) is a big statement, basically saying Britain doesn’t want to become fully dependent on American AI.

Vietnam’s Ho Chi Minh City fund and India’s NIIF show governments stepping in more directly to shape their tech and infrastructure futures.

Small Funds, Big Conviction

Some of my favorites are the tiny ones:

- BKR Capital ($15M) - Canada’s first fund for Black-led tech companies.

- Redbud VC ($25M) - betting on the Midwest and already showing strong returns from Fund I.

- 2am VC ($9.5M) - tiny India-US bridge fund trying to connect the two ecosystems early.

These shouldn’t exist by normal LP math, but they do because the GPs are obsessed with something specific.

What This Month Really Tells Us

Fund size doesn’t equal quality. Some of the smallest funds here are doing things no big fund can or will do.

Geography still matters a lot. Local teams have real advantages that outsiders underestimate.

The best operators-turned-investors aren’t always the famous ones. Real experience (like Kerrest at Okta) still carries serious weight.

And the most useful fund for you probably won’t be trending anywhere. It’ll just be the one whose thesis actually fits what you’re building.

Find full profiles, check sizes, portfolios, and contact info for all 59 funds below.

New Venture Funds - March 2026

Rows per page