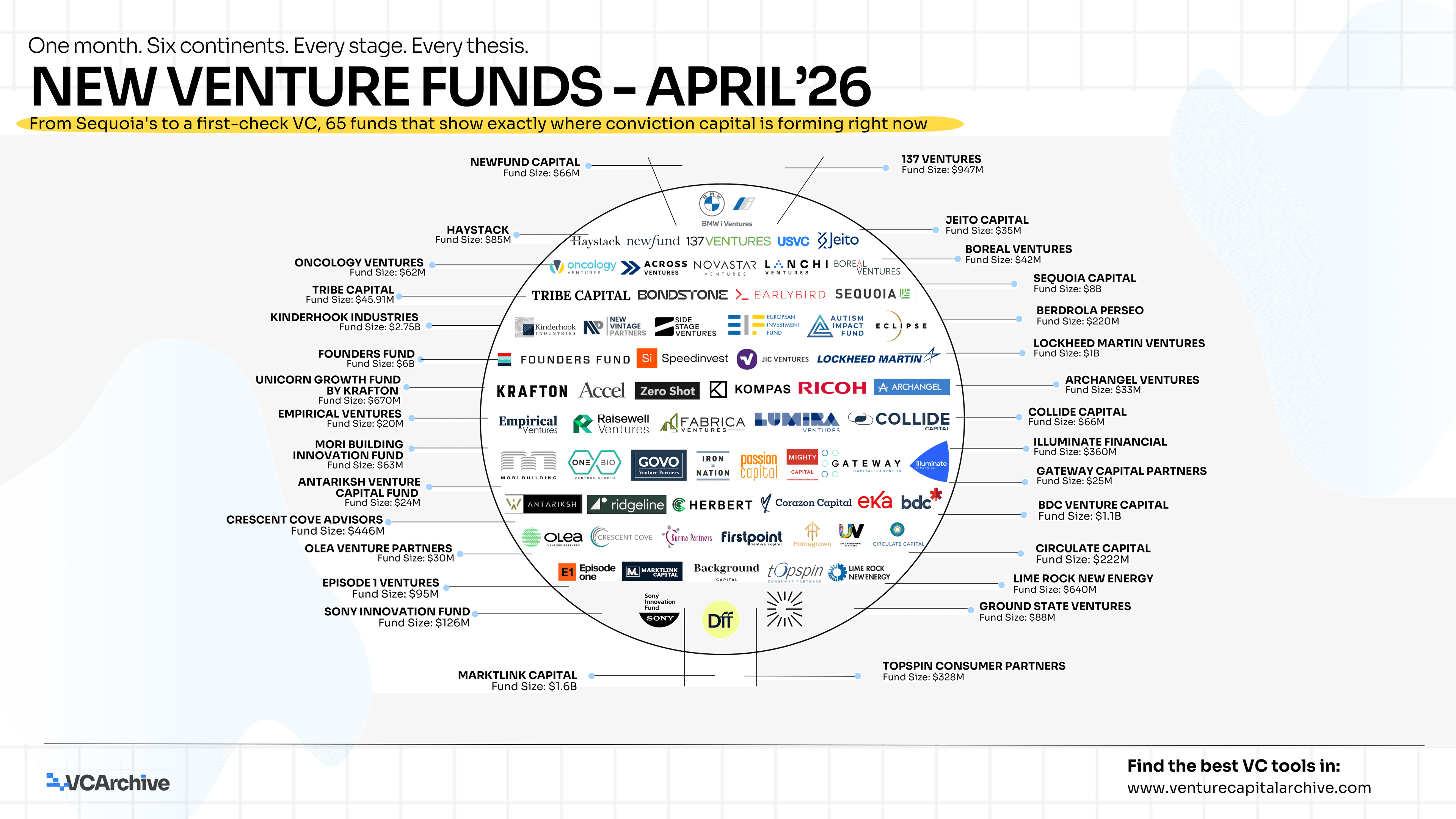

New Venture Funds - April 2026

The context you need before reading this list

Global venture capital investment more than doubled from $128.6 billion in Q4 2025 to a record $330.9 billion in Q1 2026, fueled by an extraordinary concentration of capital in large megadeals. The headlines will tell you this is an AI story. They are not wrong. But they are incomplete.

Of 1,314 funding announcements tracked in April 2026, 764 involved AI or machine learning companies. That is nearly three out of every five deals. But the more useful insight is what is happening outside that number. The other 550 deals tell a different story — one about specialisation, about emerging geographies, about defence tech and climate and biotech and industrial automation quietly attracting serious capital from serious managers who are not competing for the same AI infrastructure rounds that dominate the news cycle.

The 65 funds that closed or launched in April 2026 are a cross-section of both stories. Read them together and they form something more useful than a list. They form a map of where the next cycle of venture returns is being constructed right now.

The scale gap is real and it tells you something

The range of fund sizes on this list is striking and deliberate. At one end, the European Investment Fund closes at $16.5 billion. Sequoia raised $8 billion. Founders Fund closed at $6 billion. Accel at $1.35 billion. At the other end, Empirical Ventures in Bristol raised $20 million, Homegrown Ventures in Dubai raised $22.8 million, Archangel Ventures in Melbourne raised $33 million, and OneBio Venture Studio in Nairobi did not disclose a number at all.

That spread is not random noise. It reflects the structural reality of where venture capital is going in 2026. LP preference is consolidating around highly established fund managers at the top, while at the same time, the US saw $47.8 billion in funds raised in Q1 2026 alone, driven particularly by larger funds over $500 million. The mega-managers are getting bigger. But the emerging and regional managers are getting more interesting — because they are operating in markets and sectors where the mega-funds cannot follow, will not follow, or frankly do not know how to follow.

Smaller funds are forced to go earlier or write small participation checks. It could be a great time to be an early-stage firm if you can pick well and get in before the big uptick rounds, which are increasingly happening at the Series A stage. The emerging funds on this list understand that. They are not trying to compete with Sequoia. They are trying to find the company Sequoia will want to lead the Series B. FINTRX

The themes hiding inside the noise

Look past the AI concentration and four distinct themes emerge from this list that are worth paying close attention to.

Defence and deep tech are attracting institutional conviction. Lockheed Martin Ventures closed a $1 billion fund focused on AI, aerospace, defence, and IoT. Antariksh Venture Capital in Mumbai raised $24 million specifically for space tech, defence tech, drones, and geospatial. Ridgeline Capital in Tennessee raised $180 million for AI, advanced computing, hardware, automation, and defence. These are not peripheral bets. They are category-defining positions being taken by funds that see defence and dual-use technology as the defining investment theme of the next decade, not a niche.

Climate and energy transition capital is maturing. Lime Rock New Energy closed $640 million focused entirely on energy transition, clean energy, renewables, and EV electrification. KOMPAS VC in Amsterdam raised $187.5 million with sustainable energy as a core thesis. Speedinvest included climate tech in its $380 million pan-European fund. Emerging niches like AI-enhanced climate tech are experiencing rapid growth, and the funds on this list that sit at the intersection of AI and climate are arguably the most interesting positioning plays in the entire dataset.

Healthcare and biotech are finding their own cycle. Lumira Ventures raised $200 million for life sciences in Canada. Oncology Ventures in New York closed $62 million specifically for cancer care infrastructure. Jeito Capital in Paris raised $35 million for healthtech and biotech. Olea Venture Partners in Athens is backing medical devices and digital health. Asabys-adjacent funds like these are not chasing AI valuations. They are playing a different game entirely — one with longer timelines, higher technical barriers, and, historically, the most defensible exits. A healthcare company raising Series B in April faces longer institutional wait times than it did in 2023, pushing more healthcare founders toward growth equity, secondary fundraises, or strategic buyers. The specialist funds on this list exist precisely to fill that gap.

Geography is the most underrated signal on the list. Firstpoint VC in Istanbul raised $58 million for gaming, entertainment, and AI. Homegrown Ventures in Dubai raised $22.8 million for consumer goods and food and beverage across the Middle East. OneBio in Nairobi is building a venture studio for biotech and healthtech in East Africa. JIC Ventures in Brno, Czech Republic raised $50 million for deep tech and AI in Central and Eastern Europe. In just the third quarter of 2025, venture capital raised in the Middle East hit a record-breaking $1.2 billion driven by mega deals, and government-backed funds are injecting anchor capital into private markets across the region. The funds on this list that are planting flags in Istanbul, Dubai, Nairobi, and Brno are not taking consolation prizes. They are taking first-mover positions in markets that the mega-funds will be paying premiums to enter in three years.

What the fund structure reveals

Beyond themes, the structural mix of this list is worth reading carefully.

Corporate venture capital is having a genuine moment. Lockheed Martin, Ricoh, Sony, BMW i Ventures, Mori Building — four of the most significant corporate venture arms in the world all closed or announced funds in April. Enterprise software especially AI-driven SaaS for cybersecurity and devops is doing well, and corporates are increasingly using their venture arms as both strategic intelligence and acquisition pipelines. For a founder building in deep tech, industrial AI, or enterprise infrastructure, a CVC check from one of these names is not just capital. It is a customer validation, a distribution signal, and often the fastest path to a strategic exit.

Impact-oriented capital is professionalising. The Autism Impact Fund raised $60 million specifically for companies serving the autism community across manufacturing, consumer products, and media. Unconventional Ventures raised $92 million for agrifood, social impact, and sustainability. Circulate Capital in Singapore raised $222 million for the circular economy. The era of growth at any cost is over; 2026 venture dollars are chasing startups that solve tangible problems and can eventually stand on their own financially. The impact funds on this list are not soft money. They are applying the same return discipline to problems that most funds have never bothered to address.

The one number that frames everything

Global venture capital deployment is expected to reach the high $400 billion mark in 2026, implying a 10% increase from an already record-breaking 2025. More capital, deployed more selectively, into a smaller number of higher-conviction bets, by a wider range of fund types and geographies than at any point in the asset class's history.

That is the market the 65 funds on this list are operating in. Some are adding to pools of capital that already define the industry. Others are staking out territory that the industry will spend the next decade trying to catch up to.

The list below is not a ranking. It is not a curated top-ten. It is April 2026 in full - every fund that launched, closed, or raised, captured in one place so you can read the signal, not just the noise.

New Venture Funds - April 2026

Rows per page