Does Your Startup Need Constant Fundraising?

It may come as a shock, but not every business I have been part of was a winner.

For years, I believed that continued investor backing meant a company was thriving. Capital was the validation I was looking for. Venture capital underwriters, board members, advisors, and experienced operators endorsed the business, the vision, and the leadership. If funding kept coming, I treated the underlying model as sound and success as inevitable. When something broke, we raised. When growth slowed, we raised again. When the model strained, we assumed the next round would buy us time.

I was wrong.

I used to envy founders who inherited successful businesses or raised large rounds early because their businesses worked without constant reinforcement from capital. No 16-hour days. No constant pressure. Just steady building supported by self-sustaining models.

I confused funding with progress

I am not alone in this mistake, but that does not make it less costly.

I built real technology. In some cases, it was best in market. But I did not build a sales engine capable of supporting it. Worse, given the structure of the business, that gap may never have been closeable.

There were years the company generated millions, even tens of millions, in revenue. On paper, it looked successful. Underneath, it was fragile.

The business relied heavily on expensive human capital. People touched nearly every part of the operation, from sales to service to delivery. The company had automation, workflows, and software tools, but the most critical and expensive work still depended on people.

Customer acquisition costs were high. Retention was inconsistent. Pricing sat above the market in a crowded, commoditized industry. Every dollar of growth required disproportionate effort.

And yet, capital kept coming in.

Capital hid the flaws

Repeated fundraising does not just delay failure. It warps decision making, shifting focus from repairing weaknesses to sustaining growth.

When capital is abundant, urgency disappears. Losses feel temporary. Hard choices are postponed because the next round is expected to absorb mistakes. Cost creep is labeled investment. Cultural strain is dismissed as growing pains. Market pressure is treated as noise. Client churn is rationalized as part of scaling. Each issue feels survivable, isolated, and trivial.

Flush with capital, the company expanded three offices during COVID. There was no customer-driven demand forcing that move. It was a bet that growth would catch up to spending. Gross margin could not support operating costs without constant cash injections. New funding was required not to accelerate the business, but to keep it standing.

The illusion held as long as spending continued. When it slowed, existing weaknesses accelerated and began to compound. Growth collapsed because it had been purchased, not earned.

At the peak, the cracks were visible, but they only became impossible to ignore once capital stopped flowing.

The metrics that actually matter

Valuation was easy to talk about. The numbers told an impressive story, but the real one was ignored. When the company burned three or four dollars to generate one dollar of net new revenue, it was not scaling. It was failing. Growth was being bought, plain and simple.

Customer acquisition cost payback mattered more than topline growth. When it took longer than 12 months to recover acquisition costs, it signaled the core problem: the fragility of the company’s independent operations.

Contribution margin exposed whether the business could stand on its own. When revenue could not cover variable costs, no amount of funding could fix the model.

Cash runway felt safe. With capital in the bank, it was easy to feel secure. In reality, the company was living on borrowed time. When funding abruptly stopped, that confidence disappeared just as quickly.

The question that mattered, the one I should have asked all along, was simple. Could the business survive on its own revenue?

That was the only question worth asking. It should have been the focus from day one.

Raising capital is fun and that is the trap

Raising capital felt like winning. It was validating. It was exciting. It was addictive.

The culture around startups reinforced that feeling. Fundraising was rewarded as much as execution. Board conversations centered on runway, valuation, and the next round, not on durability, accountability, or perfecting what already worked. Capital redirected focus toward growth for its own sake. Sustaining the business, strengthening fundamentals, and pressure-testing the model were deferred in favor of expansion.

As a result, unprofitable growth was tolerated for too long. Burn was not treated as a warning. It was justified as an investment in growth and scale.

In the end, I learned that raising money was not the same as creating value. It only postponed the moment when the business had to stand on its own.

The reality check

Every founder eventually faces this moment. Either by choice or by force.

When I was forced to confront the numbers honestly, everything changed. I stopped asking how much capital the company could raise and started asking whether it could survive without it.

That shift reshaped how I evaluate companies, growth, and success.

Companies need capital. That is not the debate. But companies that rely on outside funding to stay alive are not building businesses. They are refinancing risk.

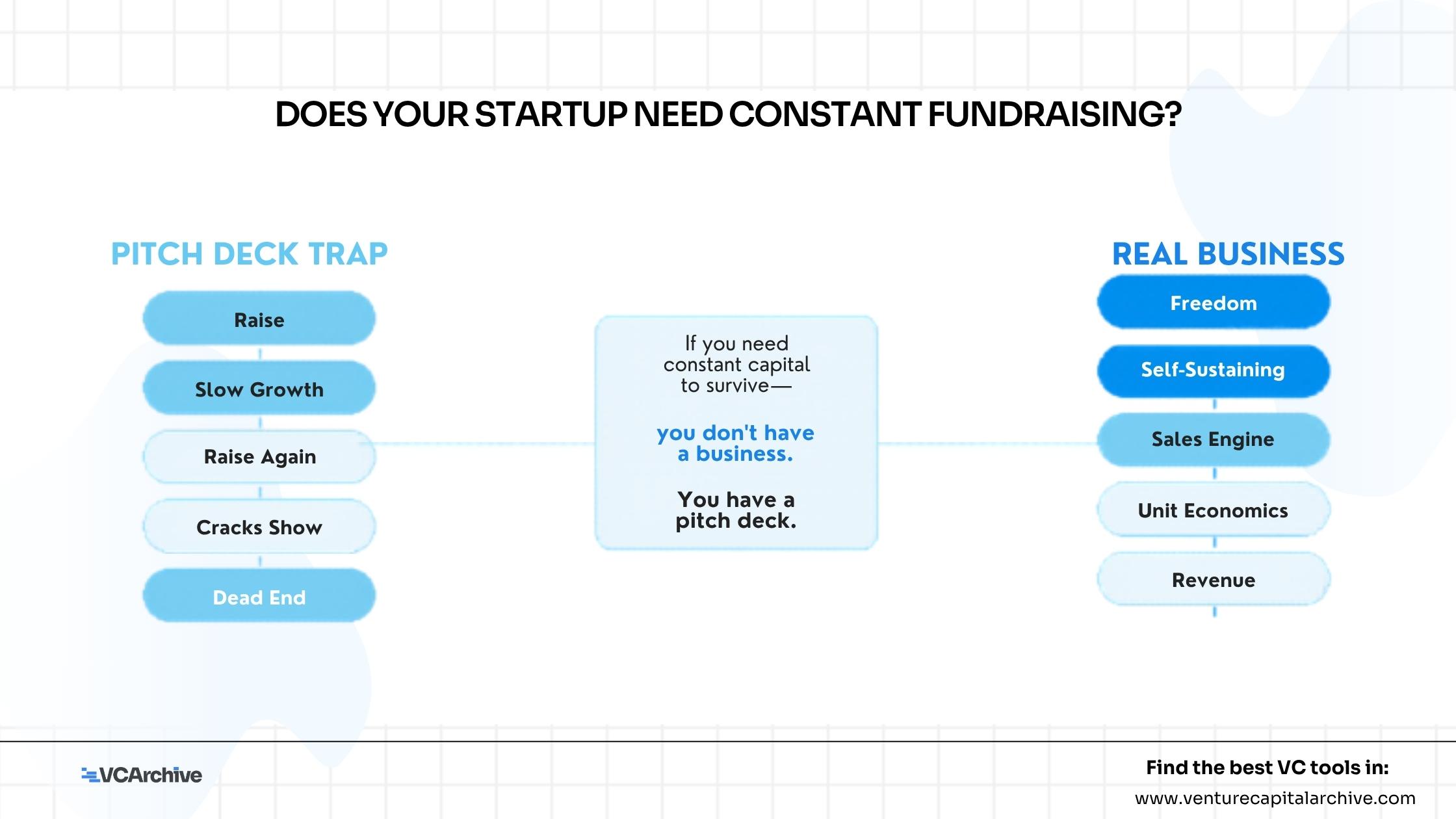

If your startup needs constant fundraising to survive, you do not have a business.

You have a pitch deck.

This article was originally published on Inc Magazine by Roy Dekel and has been sourced here for educational purposes

More from Roy Dekel

No other articles from this author yet. Visit their profile.