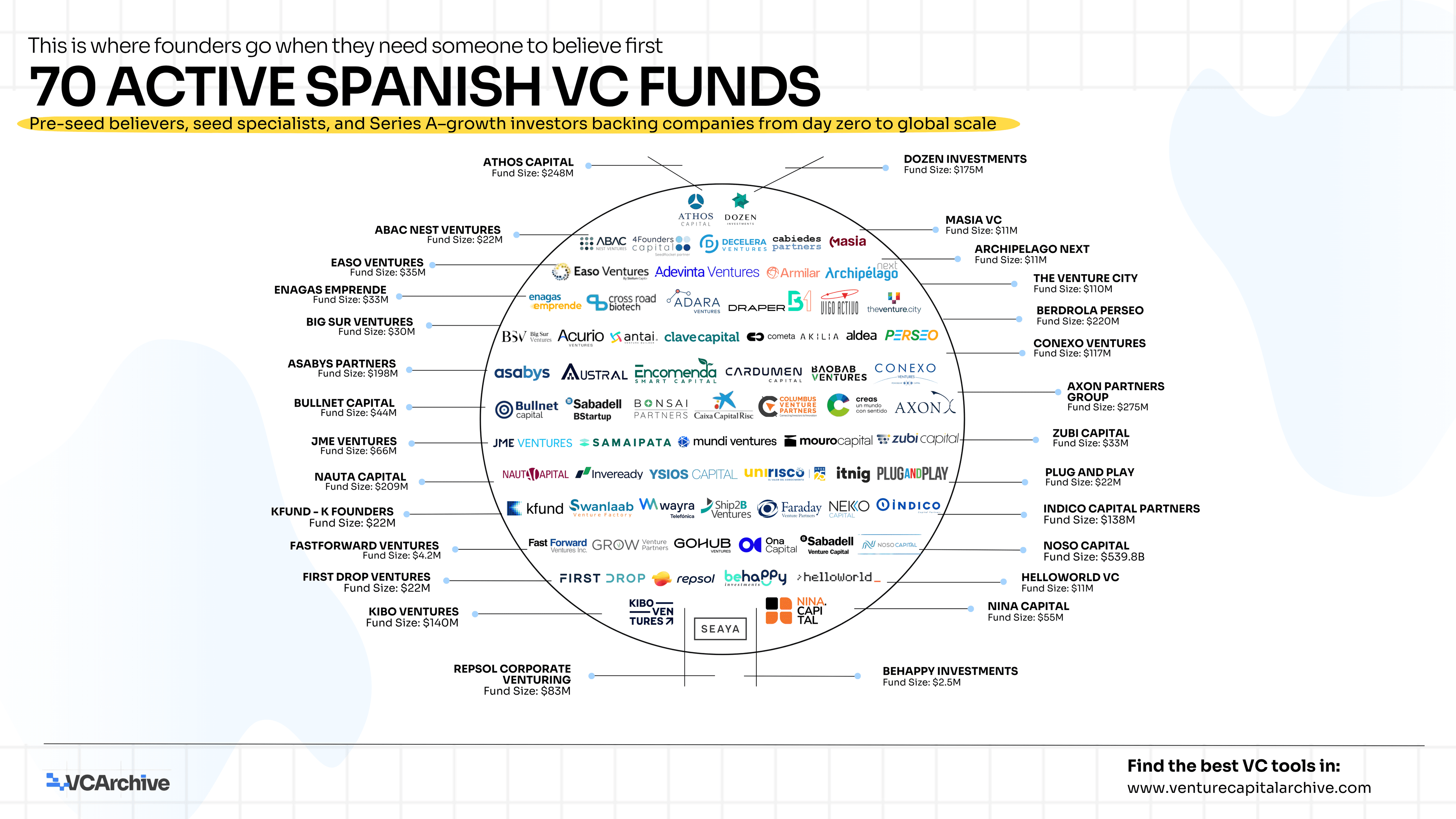

70 Active Spanish VC Funds of 2026

Spain is not emerging. It has emerged.

Spain is the second fastest-growing startup ecosystem in Europe over the past five years, surpassed only by Belgium. Let that land for a second. Not third. Not fifth. Second in Europe. And most people outside the Iberian Peninsula still talk about Spain like it is a market that is about to have its moment.

The moment already happened. The combined enterprise value of Spanish startups has more than doubled since 2020, exceeding €110 billion. 2024 became the fourth best year on record, with €1.9 billion raised. Then 2025 came along and made 2024 look modest. The first half of 2025 alone surpassed €2 billion in total fundraising, a 23% increase over the same period in 2024.

This is not a fluke. This is compounding.

What built this, and why it is different from other European ecosystems

Most European tech ecosystems were seeded by one or two companies that spawned a generation of operators who then became founders and investors. Spain has a different shape. It has several of those companies across multiple cities; Glovo, Wallapop, Cabify, Flywire, Factorial, Job&Talent and the alumni networks they created are now running funds, writing first checks, and sitting on boards across the same list you are about to read.

More than half of those who found successful startups are serial entrepreneurs. Many have worked at firms like McKinsey, BCG or Bain, or at Spanish startups like Tuenti, Carto or Geoblink, which are consolidated as great schools of entrepreneurial talent. The operator-to-investor pipeline in Spain is not theoretical. It is actively running. 4Founders Capital is literally built by the founders of Factorial, Wallapop, and Tradeinn. Itnig spawned Factorial and then became its own fund. Antai built Glovo and Wallapop and is still building today. Samaipata was co-founded by the person who sold La Nevera Roja to Just Eat.

When you look at the 70 funds on this list, you are not looking at career investors who studied finance and decided to write checks. You are looking at people who built things, broke things, scaled things, and then crossed the table. That distinction matters enormously when you are trying to raise.

The geography surprise

Ask someone outside Spain where the startup capital is and they will say Barcelona or Madrid. Ask someone inside Spain and they will give you a much more interesting answer.

In 2025, Valencia attracted €229 million in venture capital, followed by San Sebastián with €206 million, Bilbao with €68 million, and Santander with €40 million. The capital is decentralising. And the 70 funds on this list reflect that. Easo Ventures and Ysios Capital operate from San Sebastián. GoHub Ventures and Draper B1 are based in Valencia. Noso Capital covers Galicia. Vigo Activo and Unirisco are embedded in regional ecosystems that most international VCs would not be able to find on a map, let alone evaluate properly.

40% of the companies in Suma Capital's venture portfolio are headquartered outside the traditional hubs, reflecting a more diverse and specialised Spanish ecosystem increasingly supported by institutional and corporate backing.

This decentralisation is not cosmetic. It is structural. And for a founder building outside Madrid or Barcelona, it means the relevant fund may well be two hours away, not a flight away. That changes the fundraising calculus entirely.

The structure of this list is itself a story

Seventy funds sounds like a lot. It is not, relative to the size of the opportunity. Spain now has 5,010 active startups, a 38% year-on-year increase, generating over 108,000 direct jobs and €14.8 billion in annual economic impact. Seventy funds serving that many companies means the market is still undersupplied at certain stages, particularly growth.

The report highlights ongoing challenges including a lack of local growth-stage funds, a shortage of institutional investors such as insurers and corporates, and limited exits to recycle capital. That gap is real. But it is also closing. Kibo Ventures, Seaya, Nauta, and Mouro Capital are all operating comfortably in the growth zone. Mundi Ventures has built a €1.65B AUM platform around insurtech globally from a Madrid base. Inveready has deployed €2.6B across 35 vehicles over 20 years.

The fund landscape on this list breaks into roughly four types, and knowing which type you are approaching changes everything about how you pitch.

The operator funds are where Spain is genuinely different from the rest of Europe. 4Founders, Antai, Itnig, Samaipata, JME Ventures, K Fund — these are funds where the partners have personally built the kind of company you are trying to build. They will not be impressed by your deck. They will be impressed by your numbers, your customer conversations, and how clearly you understand the problem you are solving.

The sector specialists are deeper than they look from the outside. Ysios Capital has 17 years of pure biotech investing. Asabys is healthcare-only. Cardumen bridges the Spain-Israel tech corridor specifically. Adara has been doing cybersecurity and deep tech since 2005, before most European VCs knew what a CISO was. These are not generalists with a sector preference. They are specialists with two decades of domain pattern recognition. Walking in without understanding their specific thesis is a fast way to waste a meeting.

The corporate and bank vehicles deserve more credit than they typically receive. Corporate venture capital participated in 71 operations in the first nine months of 2025 in Spain alone. Wayra, BStartup, Caixa Capital Risc, Iberdrola Perseo, Repsol Corporate Venturing, Adevinta Ventures, Enagas Emprende, these are not just capital sources. They are distribution networks, customer pipelines, and market validation stamps all wrapped into one check. If your company has a natural strategic angle into Telefónica, Banco Sabadell, CaixaBank, Enagás or Iberdrola, the CVC arm of that company is not a secondary option. It is arguably a more valuable first call than any independent VC.

The emerging managers are the highest-risk, highest-relationship-intensity investors on the list. Masia VC, Baobab Ventures, HelloWorld VC, First Drop Ventures, Fastforward Ventures, these are small, lean, and deeply personal in how they invest. They have less capital but more availability. They will spend more time with you at the earliest stages than most larger funds can afford to. And for a pre-seed founder who needs an investor who will actually pick up the phone, that is not a small thing.

What the numbers say about where this is heading

Mixed investment, in which both domestic and foreign investors participate in the same round, grew nearly threefold in the first nine months of 2025, accounting for 48% of total capital. That is the single most important trend in this data. It means Spanish startups are no longer choosing between local capital and international capital. They are getting both in the same round, with the domestic VC validating for the international investor, and the international investor providing the global network the domestic VC cannot.

An estimated 70 to 80% of the funds raised by Spanish startups comes from international investors, mainly in growth funding rounds. The local funds on this list are not competing with Sequoia or a16z. They are the gateway to them. Getting the right Spanish VC on your cap table early is increasingly the most reliable path to getting a global investor at the next round.

With over 3,000 startups born in recent years, Spain's tech ecosystem boasts a robust early-stage foundation. However, the graduation rate from seed funding to Series A remains lower than the European average, a sign that scaling up is still a complex hurdle for many.

That gap between seed and Series A is where most of the value is being created and most of the risk is being taken right now. The funds that understand how to help a company bridge that gap, operationally, commercially, and in terms of network access, are the ones worth prioritising on this list.

The one thing most founders get wrong about pitching in Spain

They think the ecosystem is smaller than it is, so they underprepare. They fly in for two days, take five meetings, and treat it as a quick capital-raising sprint rather than a relationship-building process.

The Spanish VC community is not large. It is highly interconnected. The partners at the funds on this list know each other. They co-invest together constantly. They compare notes. A founder who shows up poorly prepared, or who pitches Kibo and JME with the same generic deck, or who ghosts after a meeting that seemed to go well, that travels faster than any LinkedIn post.

The founders who raise well in Spain do the same thing good founders do everywhere: they treat every conversation as the beginning of a relationship, not the execution of a transaction. They come in knowing which fund they are talking to, why, and what specifically that fund's experience makes them the right partner for this specific company at this specific stage.

That preparation is the only edge that reliably works. The 70 funds below are the starting point. The work is knowing which doors to knock on, in which order, and what to say when they open.

70 Active Spanish VC Funds of 2026

Rows per page