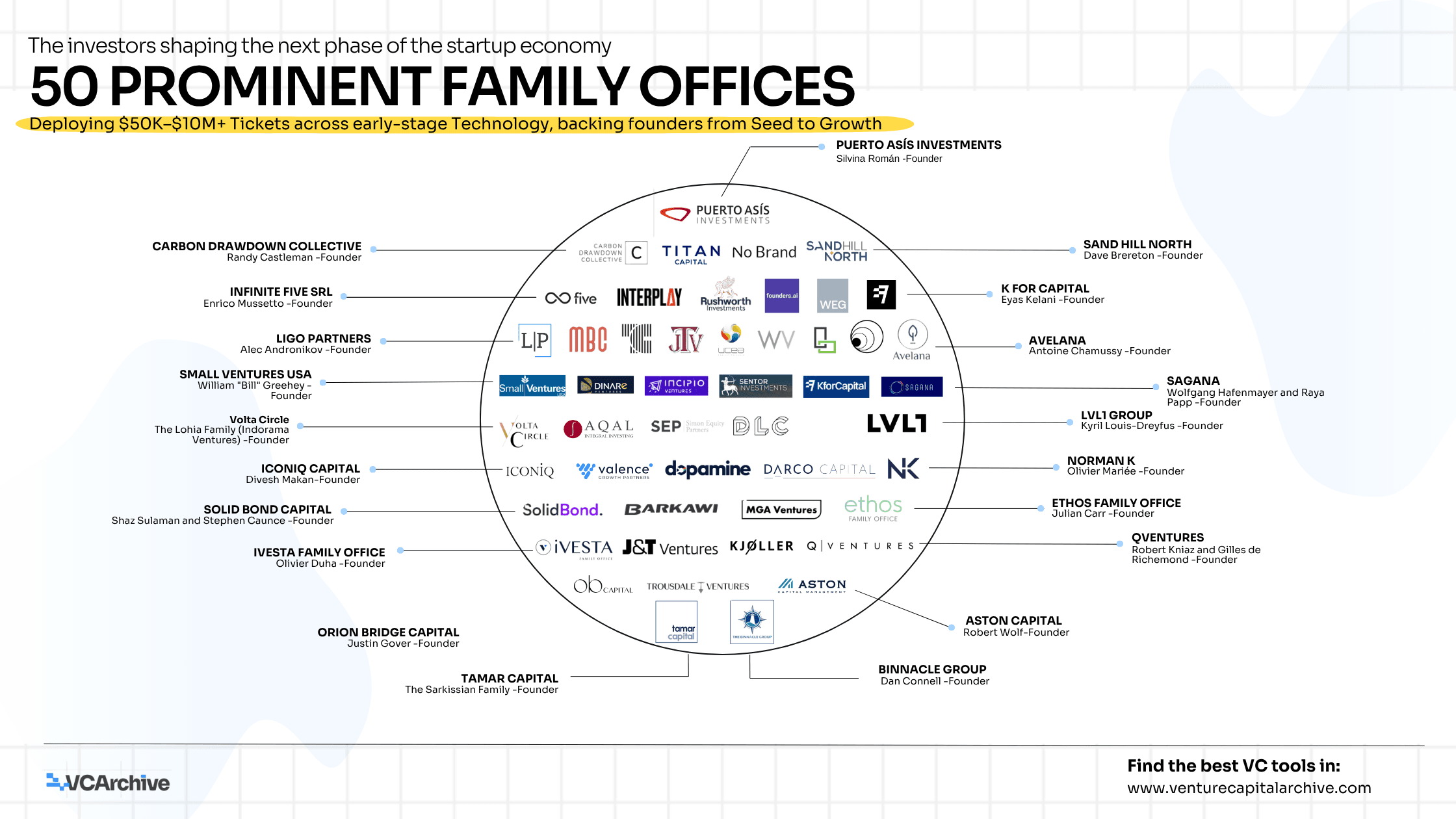

50 Prominent Family Offices actively investing in VC

The Quiet Shift Nobody Is Talking About Loudly Enough

Something structural has changed in how venture capital gets funded and it didn't happen at a press conference.

Family offices, once content to park wealth in public equities, real estate, and bonds, have spent the last decade quietly repositioning themselves as one of the most consequential LP categories in private markets. Over the past decade, family offices have increasingly favoured venture capital, whose share of their total investments rose from 17% in the second half of 2015 to 38% in the first half of 2022, settling at a healthy 31% in the first half of 2025.

That is not a trend. That is a structural reallocation and it is reshaping who funds the funds that fund the future.

According to BNY Mellon's 2025 study, family offices now allocate roughly 48% of assets to alternatives; private equity, venture capital, hedge funds, real estate, and real assets. In the US, that figure rises to 54%, underscoring how aggressively American families have shifted toward private markets.

The 50 family offices in this list are the active face of that shift. From ICONIQ Capital managing tech entrepreneur wealth across Silicon Valley, to Walerud Ventures backing Nordic seed-stage startups, to Titan Capital deploying operator capital from India's startup ecosystem - this is not a uniform category. It is a spectrum of mandates, structures, geographies, and conviction levels that collectively represent one of the most underanalysed LP pools in global venture.

What Makes a Family Office Different and Why It Matters to VCs

The instinct to lump family offices in with other LP categories misses something important. Their structural DNA is different in three ways that matter enormously to any GP trying to build a durable fund.

First, they operate on generational time horizons. Unlike institutional investors tied to quarterly reporting, family offices can hold portfolio companies longer, capturing operational improvements and sustainable growth. They measure success in decades, not quarters.

Second, they are moving from passive to active. Venture capital and private equity now make up half of family office deal activity, reflecting a strong appetite for innovation and future growth. Family offices are targeting AI, SaaS, fintech, and healthcare, where new business models and transformative impacts are emerging.

Third - and this is the strategic insight most emerging managers miss: the structure of how they deploy has fundamentally changed. According to PwC's 2025 data, a staggering 83% of family office startup deals are now structured as either co-investments or club deals. They are not just writing checks into funds. They are building proprietary deal flow, forming peer networks, and increasingly acting as lead or co-lead investors in rounds.

That changes everything about how a GP should approach them.

Who's on This List and What the Structure Reveals

The 50 family offices here span five continents and three distinct structural types: single-family offices, multi-family offices, and hybrid venture platforms. Understanding the split matters because it tells you something about decision speed, ticket flexibility, and relationship dynamics before you ever send a cold email. The dominance of single-family offices at 80% of the list is not a coincidence. SFOs tend to have faster decision cycles, fewer committee layers, and principals who can write a check based on a relationship rather than a formal investment policy statement. For an emerging GP, that matters enormously. Most sophisticated family offices prefer investing from Fund III onward, viewing this stage as the optimal balance between institutional readiness and return potential. But the SFOs on this list; particularly the emerging-tier ones like Walerud, Darco Capital, Carbon Drawdown Collective, and Dopamine Capital, are often more willing to back Fund I and Fund II managers where the economics are better and the relationship is closer.

The dominance of single-family offices at 80% of the list is not a coincidence. SFOs tend to have faster decision cycles, fewer committee layers, and principals who can write a check based on a relationship rather than a formal investment policy statement. For an emerging GP, that matters enormously. Most sophisticated family offices prefer investing from Fund III onward, viewing this stage as the optimal balance between institutional readiness and return potential. But the SFOs on this list; particularly the emerging-tier ones like Walerud, Darco Capital, Carbon Drawdown Collective, and Dopamine Capital, are often more willing to back Fund I and Fund II managers where the economics are better and the relationship is closer.

The multi-family offices tell a different story. ICONIQ, Interplay, LVL1, iVESTA, QVentures, Ligo Partners, Sentor, and Binnacle Group all operate with more formal processes, longer timelines, and broader LP constituencies to satisfy. But their aggregate check capacity is significantly higher, and a relationship with one MFO can unlock access to multiple underlying family mandates simultaneously.

How They Actually Deploy: Stage, Structure, and What the Data Shows

The most important question for any GP approaching a family office is not "how much do they have" - it is "how do they prefer to put it to work." The answer varies dramatically across this list, and mapping it properly is the difference between a warm conversation and a wasted meeting.

A few things jump out from the data immediately:

- Seed stage is by far the most contested zone, with the highest concentration of both direct leads and co-investors. This is where family office capital is most active and most competitive and where the GP-LP relationship tends to be most personal.

- Pre-seed is almost exclusively the territory of direct leads. Offices operating here; Founders.ai, Jaiatech Ventures, Carbon Drawdown Collective, Tushiconcept are functioning more like early-stage VCs or venture studios than traditional LPs. They want board seats, founder access, and hands-on involvement.

- Growth-stage family offices are almost entirely in fund LP or co-invest mode. Offices like ICONIQ, Ligo Partners, and Dinare Ventures at the growth end are writing larger checks but taking less direct involvement, they want access to deal flow without managing it themselves.

- The fund LP only category grows as you move right on the stage spectrum, which reflects a rational risk preference: at growth stage, the companies are de-risked enough that a passive position still generates returns without requiring the operational bandwidth that early-stage direct investing demands.

Nearly two-thirds of family offices anticipate making six or more direct investments in the coming year - a 10% increase compared to those reporting having done so in the past 12 months. The directional move is clear: family offices are getting more active, not less, and the offices on this list are at the leading edge of that shift.

The Sectors They're Chasing and the One They're Ignoring

Across the 50 offices, sector concentration mirrors broader market trends but with one notable deviation. AI, SaaS, fintech, and consumer tech appear consistently across mandates. Nearly 60% of family offices believe there is a strong opportunity in AI and technology investing, versus 40% of the broader institutional investor group - a gap that reflects family offices' significantly higher likelihood of investing in venture capital, where emergent digital technology is a prominent theme.

Climate tech is the interesting anomaly. Only a handful of offices on this list; Carbon Drawdown Collective, SAGANA, and partially Avelana have genuine climate mandates. The big money in climate-adjacent family office capital appears to be flowing toward real assets and infrastructure rather than early-stage climate tech. For any climate-tech founder or fund manager reading this: the competition for these LPs is thinner than you think. A targeted approach to the three climate-focused offices on this list will go further than a broad sweep of the full fifty.

The geography tells a complementary story. North America dominates by volume, but the European cluster; Avelana, SAGANA, AQAL Capital, Kjøller, No Brand, Volta Circle, iVESTA, Warsaw Equity Group, Walerud, QVentures, UCEA is more diverse in mandate and more thesis-driven than the US contingent. The Asia presence is smaller but high-conviction: Titan Capital (India, founder-operator led), Jaiatech (India, deep-tech focus), JT Ventures (India, consumer), Valence Growth Partners (India/US), and Tushiconcept (Singapore, Southeast Asia) all represent family capital that is deeply embedded in regional ecosystems and unlikely to respond to generic outreach.

How to Actually Get a Meeting

The approach guidance embedded in this dataset is some of the most actionable data on the list. Across the 50 offices, three channels dominate: LinkedIn DM, warm introduction via network, and direct email. Only a handful list open application processes.

What family offices want from GPs is not complicated: clarity, transparency, co-invest access, and operational polish. The GPs who show up ready, who understand family office psychology, respect their process, and offer substance beyond the pitch will raise faster, build deeper relationships, and find LPs that stick across vintages.

Three things the data tells you that most pitch decks ignore:

Offices with named contact emails are meaningfully more approachable than those listing only generic inboxes. A named contact is a signal that someone is actively reading deal flow submissions. Generic inboxes often go to compliance or admin.

Multi-family offices require longer runways and operate with investment committees and formal review processes. Budget 6–9 months for a first close with these offices. Budget 2–3 months with a single-family office whose principal is the decision-maker.

Impact-rated offices respond to mission-first framing and have explicit ethical ratings in their profiles. Approaching them with a pure-returns pitch is a mismatch signal, not a feature. Lead with impact, back it with returns data.

The Bigger Picture

In the first half of 2025, while family offices saw a reduction in overall deal volume, their aggregate sales revenues surged by a remarkable 97.4% compared to the first half of 2023 - a clear signal that the focus has shifted to closing more profitable, more deliberate deals rather than maximising deal count.

Family offices are prioritising quality over quantity. Deal volume has reached a decade low, reflecting sharper selectivity in the types of transactions they pursue. Rather than spreading capital across many ventures, family offices are concentrating resources where deep expertise and active engagement promise greater value.

For founders and GPs, that means one thing above all: the era of spray-and-pray LP outreach is over. A warm introduction to one well-chosen family office on this list, with a pitch that speaks directly to their mandate, their stage preference, and their co-invest appetite is worth more than a hundred cold emails to the wrong inboxes.

The 50 family offices in this database are not the loudest voices in venture capital. But in a market where the loudest voices are often the least useful ones, quiet, patient, long-horizon capital may be exactly what you need on your cap table.

Sources: VCA 2025 Annual Report, PwC Global Family Office Deals Study 2025, BNY Mellon 2025 Single Family Office Report, UBS Global Family Office Report 2025, PwC Global Family Office Deals Study, VC Lab Family Office Investment in VC Report 2025.

50 Prominent Family Offices actively investing in VC