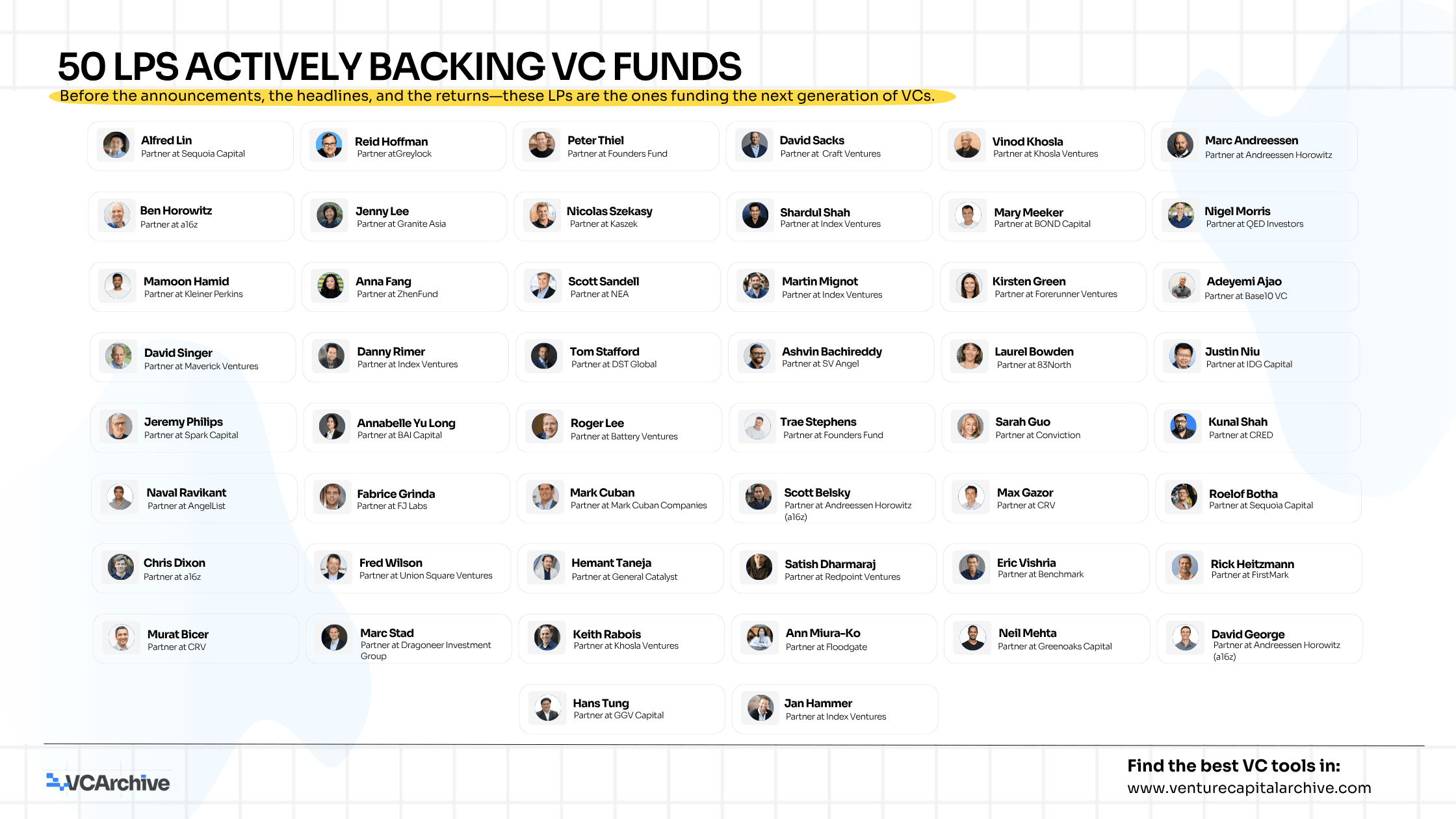

50 LPs actively backing VC funds

The venture capital ecosystem runs on two engines: the founders who build, and the capital allocators who back them. Limited Partners behind the funds rarely get the spotlight, yet their conviction shapes which technologies get funded, which geographies attract capital, and which sectors define the next decade.

This list of 50 active LPs offers a window into the minds and mandates of the people most responsible for where innovation capital flows. Here's what the data tells us and what the 2025 market is confirming.

The Market Context: 2025 in Numbers

The headline of 2025 looks like recovery. The fine print tells a different story.

Venture and growth investors poured $425 billion into more than 24,000 private companies in 2025 - up 30% year over year. Yet deal count fell sharply, with year-over-year growth concentrated almost entirely in the largest rounds and in AI. As VCA's own 2025 Annual Report put it bluntly: the industry didn't grow, it concentrated. Five companies absorbed 20% of all capital deployed globally. Strip them out, and the broader market is flat at 2023 levels. Mega-funds above $10B increased their share of industry assets from 33% to 42% in twelve months, while 574 firms quietly transitioned to zombie status - a 50% increase year-over-year.

For LPs, the consequence is clear. Global VC fundraising hit a multi-year low of approximately $86.7B as of late 2025, pushing LPs to concentrate commitments into fewer, higher-conviction relationships. The 50 names on this list are exactly those relationships - the managers and allocators still actively deploying with purpose and track record.

Who's on the List and What They Signal

The 50 LPs span a broad spectrum of mandates, geographies, and check sizes from $50K angel tickets to $100M growth rounds. The geographic breakdown is shown above. A few patterns stand out immediately.

The operator premium is real. Alfred Lin ran Zappos. Roelof Botha was PayPal's CFO. Nicolas Szekasy took MercadoLibre to Nasdaq. Kunal Shah built CRED to unicorn status. They don't just evaluate companies, they've lived the realities that make or break startups at every stage. The PayPal Mafia alone accounts for five names on this list: Peter Thiel, Reid Hoffman, David Sacks, Roelof Botha, and Keith Rabois, all still actively deploying capital, still opening doors no check size alone can substitute.

Asia is underrepresented but outsized in impact. Eight of the 50 LPs are based in Asia. Jenny Lee at Granite Asia, Anna Fang at ZhenFund, Tom Stafford at DST Global, Hans Tung at Notable Capital among them. Collectively, their portfolios include ByteDance, Meituan, Xiaomi, Grab, and Alibaba. Meanwhile, VC investment in Asia remained near multi-year lows in 2025, with China hitting its lowest level in over a decade at $4.7B in a single quarter. The relative scarcity of Asia-based LPs on global lists is both a structural gap and a contrarian opportunity.

Europe's LP voice is growing. Index Ventures alone contributes four names; Shardul Shah, Martin Mignot, Danny Rimer, and Jan Hammer - underscoring that London has evolved from a regional hub into a globally relevant capital center. In Europe, AI-focused defencetech raised significant rounds in 2025, including Germany-based Helsing at $683M and Portugal-based Tekever at $500M, signaling that European LPs are increasingly comfortable backing frontier tech at scale.

Sector Concentration: Where Conviction Is Deepest

Fintech and SaaS dominate because both sectors offer defensible recurring revenue, global scalability, and proven exit paths. AI has surged as the biggest force behind VC's rise in 2025 representing more than a quarter of total global VC funding, up from 15% in 2024 and just 7% in 2023. That shift is visible directly in this list: Sarah Guo's Conviction fund is built entirely on an AI-first thesis, Chris Dixon threads crypto and AI at a16z, and Vinod Khosla has championed deep tech and AI for two decades.

Investment trends evolved rapidly in 2025, with VC investors shifting away from broad-based investments and increasingly focusing on backing proven AI innovators with not only transformative but defensible business models, ones that cannot easily be replaced by the next AI startup. The LPs on this list embody that shift. They are not chasing hype; they are building concentrated conviction in themes they understand deeply.

The Concentration Imperative: What LP Behavior Tells Us

Perhaps the most important signal from this list isn't what these LPs invest in, it's how they operate. Across all 50, the defining trait is selectivity combined with longevity. Alfred Lin has been at Sequoia for 15 years. Danny Rimer at Index for 22. Satish Dharmaraj at Redpoint for over 20. Fred Wilson co-founded Union Square Ventures in 2003 and is still writing checks today.

This staying power matters because the defining feature of LP behavior in 2025 is selectivity: fewer manager relationships, more concentration in durable themes, and a stronger preference for structures that manage liquidity risk. Fundraising remains difficult at the aggregate level, but capital is available for scaled, differentiated platforms.

Secondary transaction volume is projected to exceed $210 billion in 2025 largely due to LPs and GPs increasingly turning to secondaries as an established avenue for liquidity. This tells you where pressure is: even the best-run funds are managing vintage portfolios in a constrained exit environment, making the track records and network depth of LPs on this list more valuable than ever as signals of where durable capital lives.

How These 50 LPs Map Across the Investment Lifecycle

The third visual below maps all 50 LPs by their primary stage focus, showing where operator-LPs cluster versus where purely institutional capital concentrates.

The stage map above reveals something important: early stage remains the most crowded zone, with 18 of the 50 LPs operating primarily between Seed and Series B. This is where operator-turned-investor leverage is highest and where, per OECD data, early-stage VC deal count reached a historic high of over 75% of all AI deals in 2025, even as mega-deals skewed the value figures. The volume is in its early stage. The dollars are in growth. The LPs on this list cover both ends.

What This Means for Founders and Fund Managers

For founders seeking capital, and for emerging fund managers building LP bases, this list is more than a directory, it is a map of where earned conviction lives in 2025.

The median time-to-close for VC fund raises is now approaching 15 months, with average cycles extending beyond 17 months. In that environment, warm introductions through shared networks - the Sequoia network, the PayPal Mafia, the Stanford GSB cluster are not soft advantages. They are structural prerequisites. Every LP on this list lists "warm intro" as the preferred approach, and that is not an accident.

The most actionable insight from this dataset: sector alignment is table stakes. What differentiates a conversation with an LP at this level is a founder or GP who understands the LP's operator history and can speak directly to the parallels between their own company and the LP's prior experience. Alfred Lin wants to hear about founder-market fit echoing his own Zappos journey. Nigel Morris wants fintech founders who understand credit the way he built it at Capital One.

Know who you're walking into a room with. That preparation is what separates a check from a pass.

Data sourced from the Venture Capital Archive curated LP database, VCA 2025 Annual Report, Crunchbase 2025 Year-End Report, KPMG Q4 2025 Venture Pulse, Bain & Company Global VC Trends 2025, and OECD AI Investment Report 2025.

50 LPs actively backing VC funds